Does the 183-day rule apply differently to Singapore company directors?

Yes. While the 183-day threshold itself applies, the administrative concessions IRAS offers to foreign employees — including the two-year and three-year concessions for those whose employment straddles calendar years — explicitly exclude directors of a company. Directors must meet the day-count threshold on a year-by-year basis without access to those concessions.

Can a Singapore company lose its tax residency if its directors travel frequently?

It can be at risk. Singapore corporate residency is based on where control and management are exercised. This is typically the location of board meetings and strategic decision-making. If directors are frequently outside Singapore, this can affect whether the company qualifies as a Singapore tax resident and whether it can obtain or retain a Certificate of Residence for double tax treaty purposes.

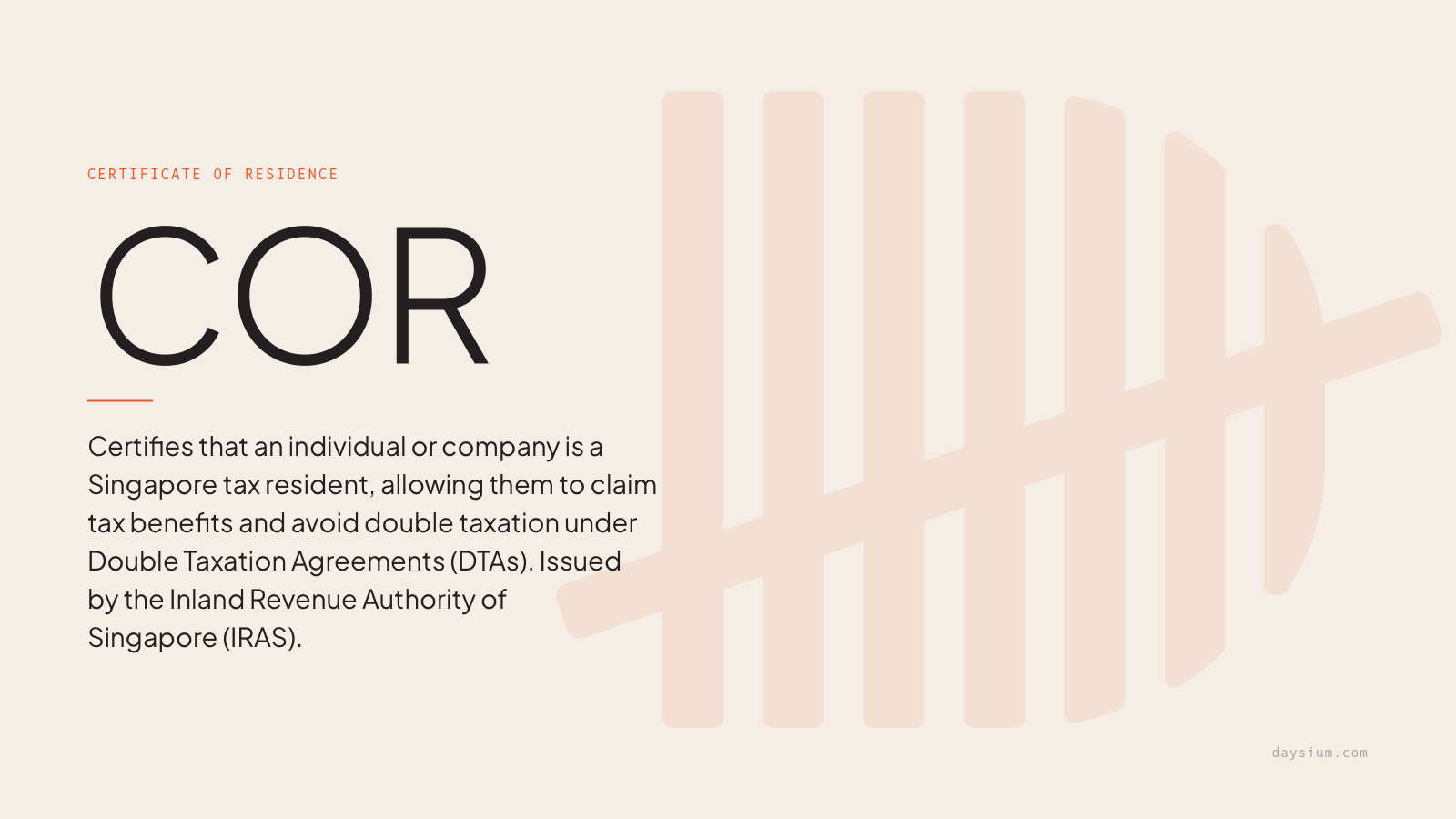

What is a Certificate of Residence, and why does it matter?

A Certificate of Residence is issued by IRAS to confirm that a company is a Singapore tax resident for the purpose of accessing double tax treaty benefits. Without a valid COR, a company cannot claim relief from withholding taxes and other levies in treaty partner jurisdictions. From 2025, IRAS has tightened the substance requirements for COR eligibility, particularly for foreign-owned holding companies.

How are directors’ fees taxed if a director is not a Singapore tax resident?

Non-resident directors are generally taxed on directors’ fees at a flat rate of 24%, regardless of how many days they spend in Singapore. Unlike employment income, directors’ fees are taxable in Singapore irrespective of physical presence, and the location of the board meeting is not determinative. This is a further reason why residency status matters: resident directors are taxed at progressive rates and have access to personal reliefs, which can make a material difference to overall liability.

Do virtual board meetings count for Singapore corporate residency purposes?

Yes, but conditionally. IRAS recognises virtual board meetings, but only treats them as Singapore-based if at least 50% of the directors with authority to make strategic decisions — or the chairman — are physically in Singapore at the time of the meeting. Directors who are frequently abroad may affect this balance, particularly on smaller boards.

What records does a Singapore company director need to keep?

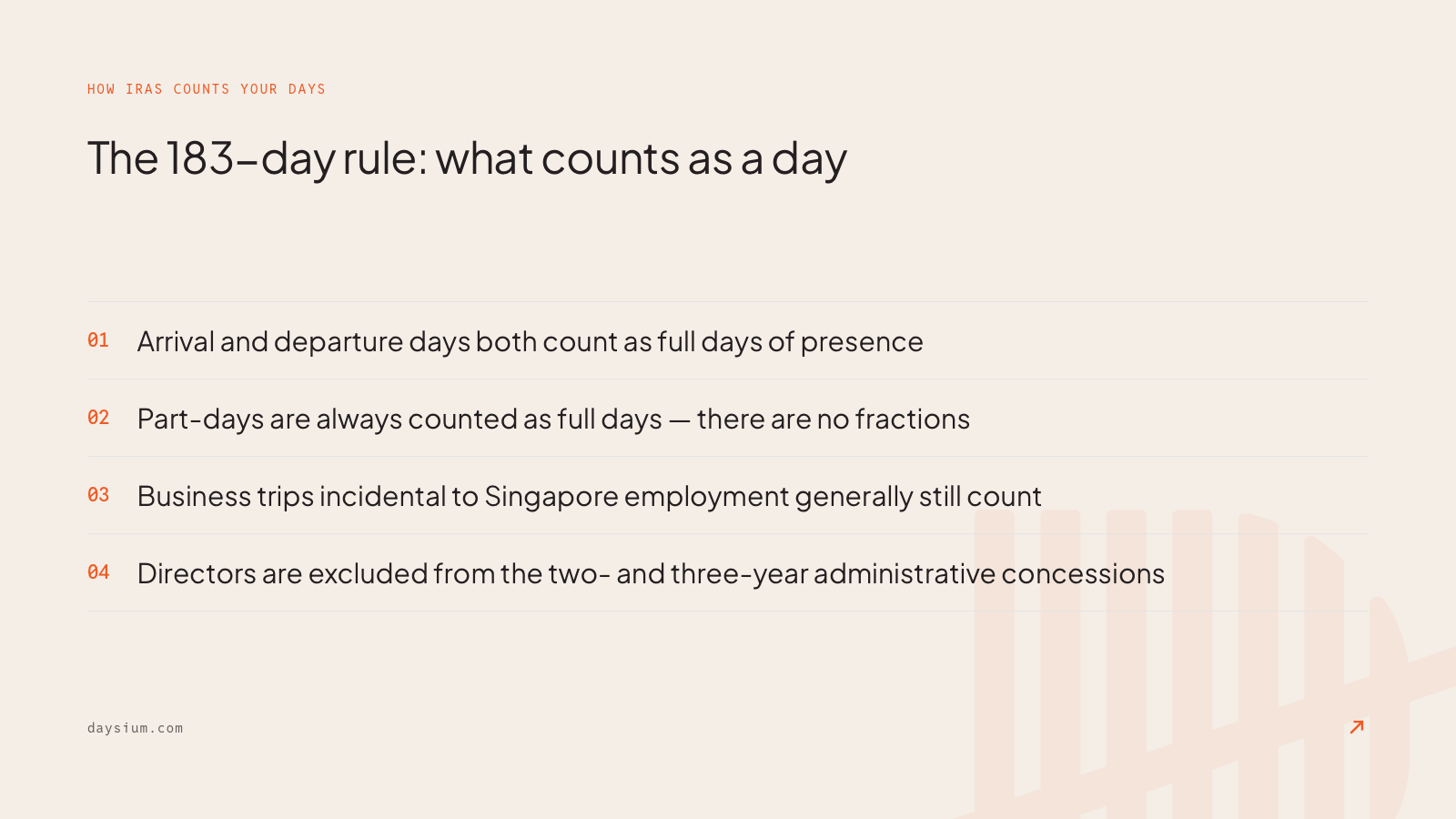

Directors should maintain contemporaneous, day-by-day records of physical presence across jurisdictions. Both arrival and departure days count as days of presence in Singapore, and part-days are counted as full days. Board meeting documentation should confirm the physical location of each director present. Records created at the time carry significantly more weight with IRAS than reconstructions prepared after the fact.