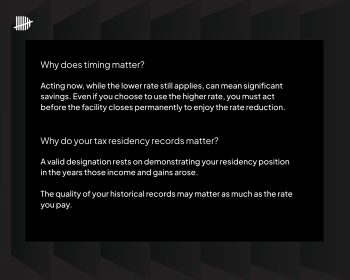

This is where the TRF intersects with something many HNWIs have underestimated for years. The quality of your historical residency records may be the single most important factor in determining whether your designation holds up under scrutiny.

The evidence requirement is retrospective

To make a valid TRF designation, you are electing to pay a reduced rate on foreign income and gains that arose in specific prior years when you were subject to the remittance basis. HMRC will scrutinise that basis. The question is simple: were you actually subject to the remittance basis in the years those income and gains arose? The answer depends on your residency status in those years, which depends on your day counts.

For continuously UK resident individuals, this is straightforward. But for globally mobile individuals, those who split their time between jurisdictions, had split years, or whose residency in particular years was anything other than clear-cut, the historic residency position is precisely what HMRC will examine.

What weak records actually risk

A TRF designation of £3 million of pre-April 2025 foreign gains is not a trivial filing. Weak historical records do not just create inconvenience. They can turn a designation into a tax investigation. And these investigations are expensive, time-consuming, and stressful even when the underlying position is compliant and correct.

Demonstrating residency status for prior tax years requires evidence that many HNWIs have not maintained in a structured way: day-by-day travel records with corroborating documentation, location data confirming physical presence on particular days, contemporaneous records such as boarding passes, hotel receipts, and geo-tagged entries. A reconstruction assembled after the fact does not carry the same weight as a record built in real time.

What strong records make possible

HNWIs who have maintained rigorous, contemporaneous residency records are in a fundamentally different position. Their historic positions are defensible. An enquiry, if it comes, can be resolved quickly and with confidence. For individuals who have used Daysium to log and evidence their movements over prior years, this position is already in good shape.

For those who have not, the period before a TRF designation is filed is the time to review existing records, identify any gaps, and work with an advisor to assess whether the evidential foundation is sufficient.