Do I still pay tax in the UK if I move abroad?

Not necessarily. It depends on your residency status and the nature of your income. UK-source income may remain taxable even after you leave, and the year of departure has specific rules under the split-year treatment provisions. A tax advisor can help clarify your position for the specific year you move.

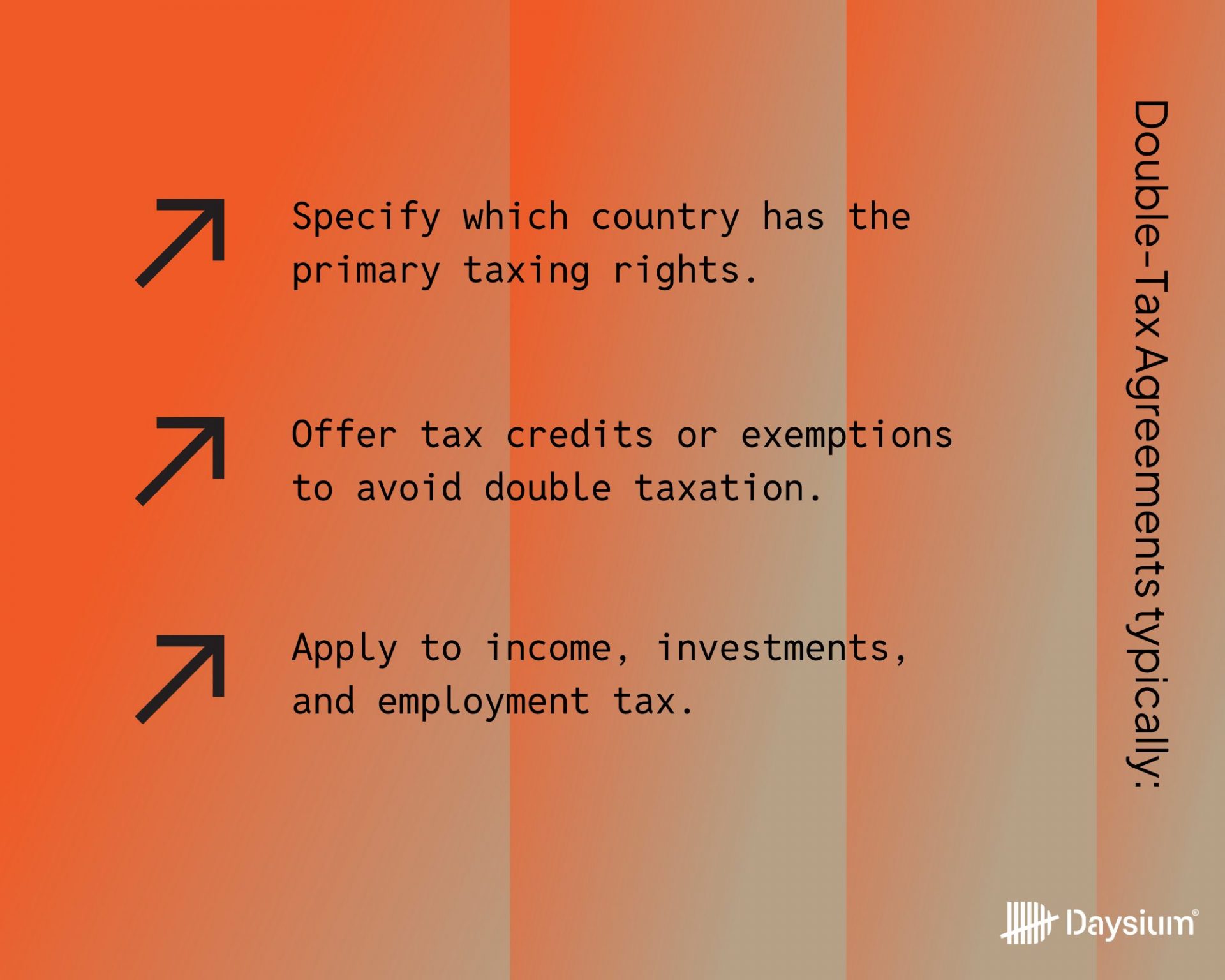

What is a Double Taxation Agreement (DTA)?

A DTA is a treaty between two countries that sets rules for which country has the right to tax specific types of income. The goal is to prevent the same income being taxed twice. However, DTAs do not automatically resolve every double taxation scenario, and the application depends on the specific countries involved and your personal circumstances.

How many days can I spend in a country before becoming a tax resident?

The threshold varies by jurisdiction. Many countries use 183 days as a trigger, but some have lower thresholds, additional “connecting factor” tests, or both. The UK’s Statutory Residence Test, for example, uses a sliding scale depending on how many UK ties you have. Accurate day counting is essential for anyone who splits their time across multiple countries.

What records should I keep when relocating abroad?

You should aim to maintain contemporaneous records of where you spend each night, evidence of travel (boarding passes, hotel receipts, bank statements), and documentation of economic ties in each country. Tools like Daysium allow you to log days automatically and attach supporting evidence, creating an auditable record that is ready to share with advisors or tax authorities if needed.