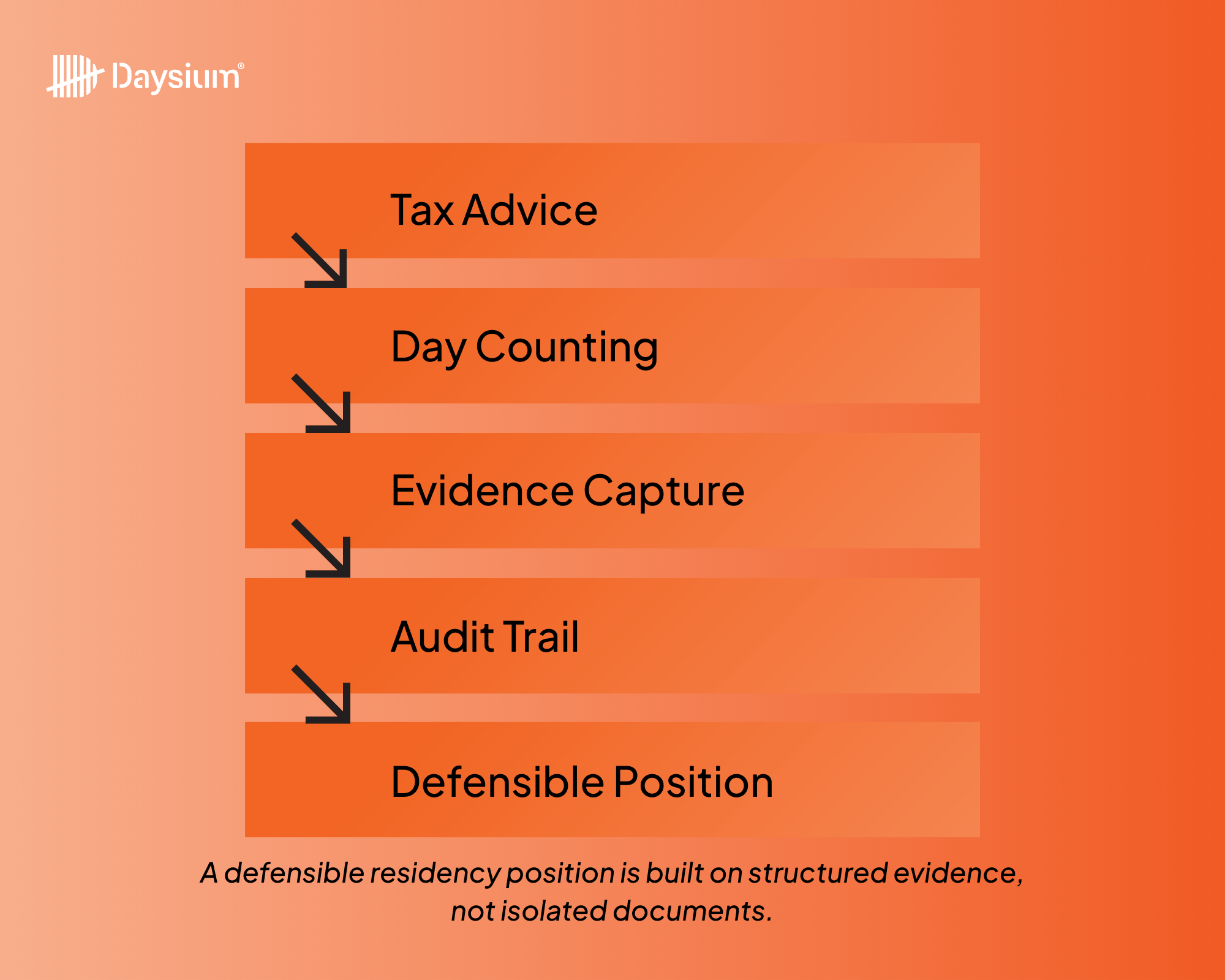

For tax advisors building a reputation in cross-border work, this is not a minor operational detail. It is a positioning issue. Clients expect clarity, authorities expect evidence, and advisors sit between the two.

If your advice is strong but the client’s process is weak, the weakest link defines the experience. If both are strong, the enquiry, if it ever comes, becomes shorter, calmer, and more predictable.

That distinction matters for client retention, firm reputation, time allocation, and stress levels during peak periods.

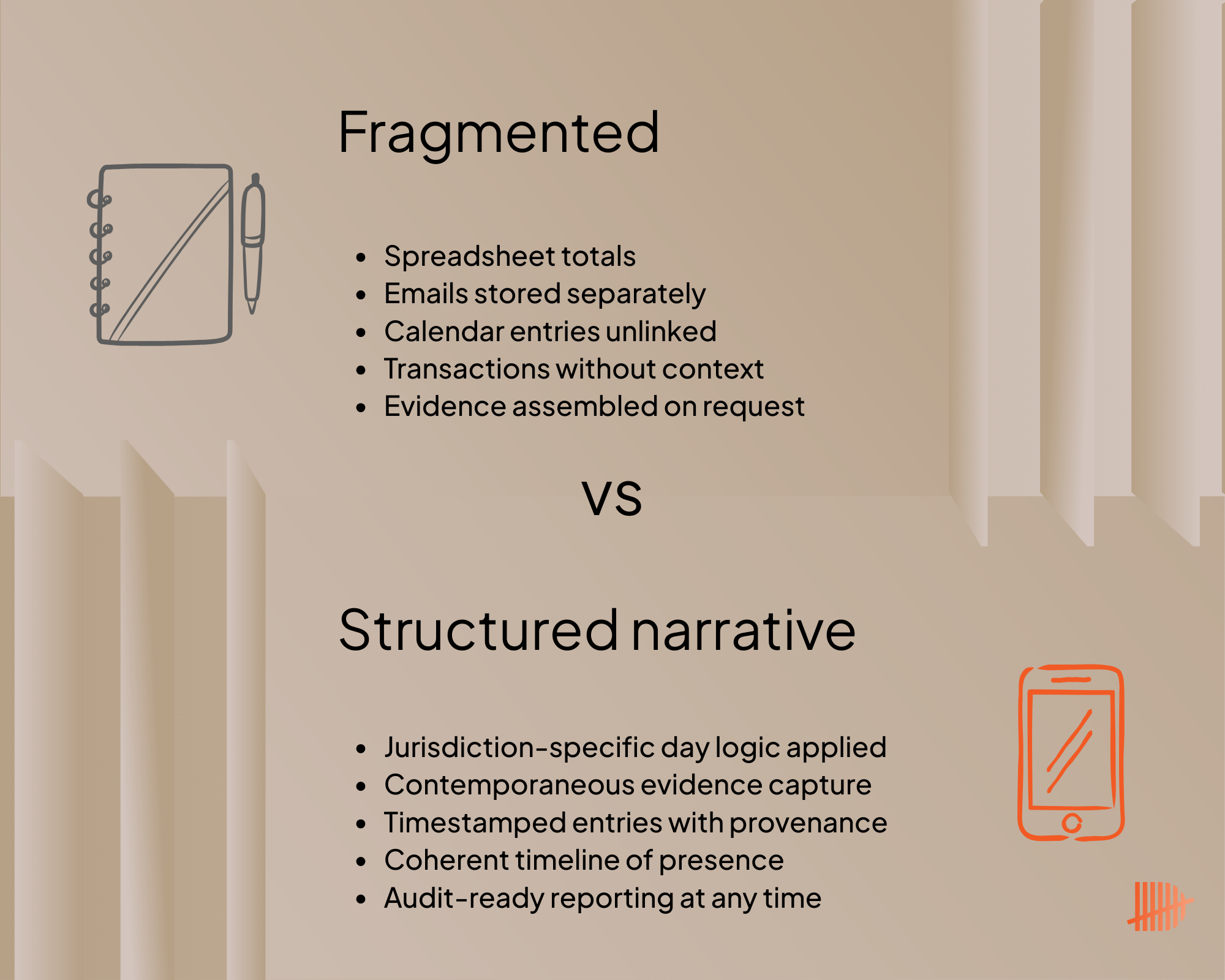

Adding narration to record-keeping

“Keep records” used to be a sufficient shorthand for tax residency record-keeping. In 2026, it isn’t. Advisors who stand out are the ones who can say: “Here’s the residency strategy. Here’s the process that supports it. And here’s the evidence trail we’ll have if anyone asks.“

That shift, from informal record-keeping to structured evidential narrative, is what transforms residency advice from technically correct to operationally defensible. And increasingly, that’s what sophisticated globally mobile clients expect.

If you’d like to discuss how to strengthen how your clients keep records for tax residency, get in touch with our team.

Book a call for a confidential meeting.