The Family Office Guide to Bulletproof Tax Residency Records

01 Sep 2025

Family offices manage wealth, safeguard reputations, cross-border structures, and tax compliance. Today, bulletproof tax residency records are essential to defend against audits, satisfy CRS/FATCA reporting, and support trusts and holding companies. With growing scrutiny in Europe and beyond, family offices that automate day counting, maintain strong evidence, and centralise compliance files can plan with confidence and protect the family’s legacy.

Family offices exist to bring clarity, efficiency, and control to the financial and personal affairs of wealthy families. From investment management to philanthropy and estate planning, they coordinate the complex web of a family’s interests. But increasingly, one issue cuts across everything a family office touches: tax residency.

In an era of heightened scrutiny, authorities from London to Monaco to Dubai are examining where individuals, trusts, and holding companies are truly resident. For family offices, this means that maintaining bulletproof residency records isn’t a box-ticking exercise. It’s a cornerstone of protecting the family’s wealth, privacy, and reputation.

Why Tax Residency Records Matter to Family Offices

Five core issues make tax residency records a vital issue for family offices:

1. Protecting the Principals

For the family itself, tax residency determines things such as income tax and inheritance tax. The concept of tax residency goes beyond keeping a spreadsheet of day counts, with authorities examining:

Where is the individual’s main home

Where else do they own properties

The centre of their vital interests, including family ties, economic, and social ties

Without robust records, families risk disputes over dual residence and unintentional tax liabilities.

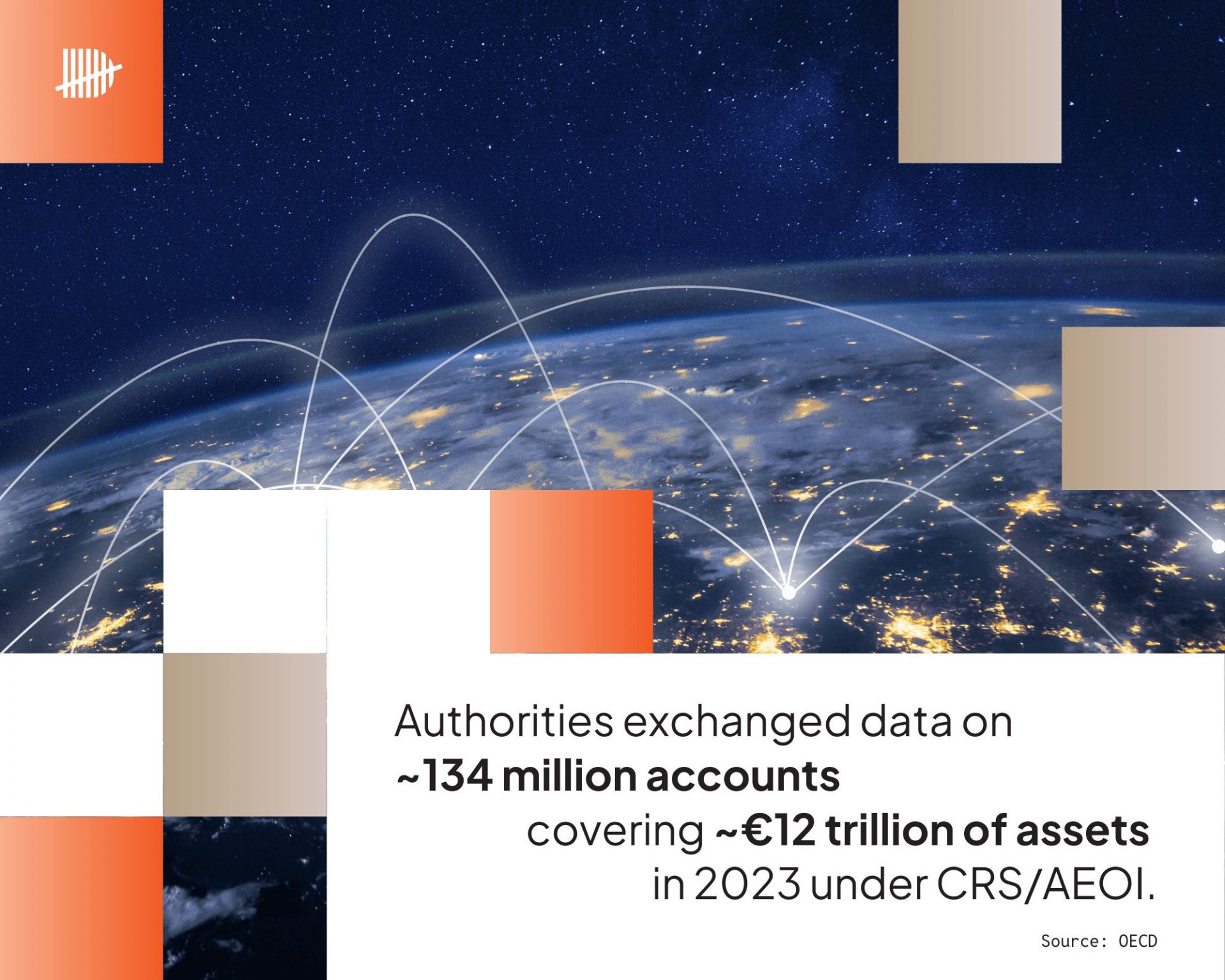

2. Certifying Residency for Banks and CRS/FATCA

Family offices act as the hub for banking, investments, and trust structures. Banks require validated self-certifications of tax residency for account holders and controlling persons under the OECD’s Common Reporting Standards (CRS) and US/UK FATCA rules. Inaccurate or outdated certifications can:

Trigger incorrect reporting to foreign tax authorities.

Cause banks to freeze accounts until clarification is provided.

Open enquiries that drag the family into lengthy explanations.

3. Trusts, Foundations, and Holding Companies

Where entities are managed and controlled is just as important as where family members reside. Courts and tax authorities expect to see meeting minutes, director travel records, and proof of decision-making in the declared jurisdiction. Weak evidence risks:

Loss of “substance” claims in holding structures.

Reclassification of income and gains as taxable elsewhere.

Exposure to inheritance tax where exemptions could otherwise apply.

The reporting duties and regulatory pressure around family offices, trusts, and holding companies are increasing.

In Europe, a reform package was passed in July to create a new Anti-Money Laundering Authority (AMLA). This new organisation is tasked with creating a comprehensive AML/CFT rulebook that aims to harmonise rules around key areas, including beneficial ownership registers and customer due diligence. While AMLA won’t directly supervise family offices, the reforms emphasise growing cross-border cooperation and information sharing.

4. Managing Risk During Investigations

Wealthy individuals are a key target for tax authorities, with dedicated investigation units across Europe. In the UK, for instance, HMRC launched a Wealthy Team unit in 2017 which has seen increasing resources. In 2023-24, compliance activities for wealthy individuals cost £350 million, up from previous years. Furthermore, additional revenue secured from wealthy individuals more than doubled from £2.2billion in 2019/20 to £5.2 billion in 2023/4 showcasing their focused efforts of scrutiny.

A family office’s ability to present consistent, contemporaneous residency records can shorten enquiries and avoid the costs, stress, and reputational damage that accompany them.

5. Efficient Planning

Overall, a clear overview of tax residency records provides a framework for more effective planning, whether for personal or wealth management purposes.

Family offices that assist with travel planning will find real-time records a timesaver. Future trips and their potential tax compliance implications can be assessed at the time of booking, rather than as an afterthought.

For wealth management, a clear understanding of tax residency ensures that appropriate tax obligations are fulfilled. The impact of future changes to tax residency can be analysed simultaneously with plans of relocation or establishment of business or trust structures in new jurisdictions.

Building the Family Office Blueprint for Residency Compliance

To protect the family, a modern family office should:

Automate: Use technology to capture day counts in real time.

Evidence: Pair days with corroborating proof.

Prepare: Keep residency packs for each family member and structure, ready for auditors or banks.

Review: Work closely with tax advisors to ensure records align with changing local rules.

What Bulletproof Records Look Like

Let’s take a closer look at how to put the four-step blueprint into action.

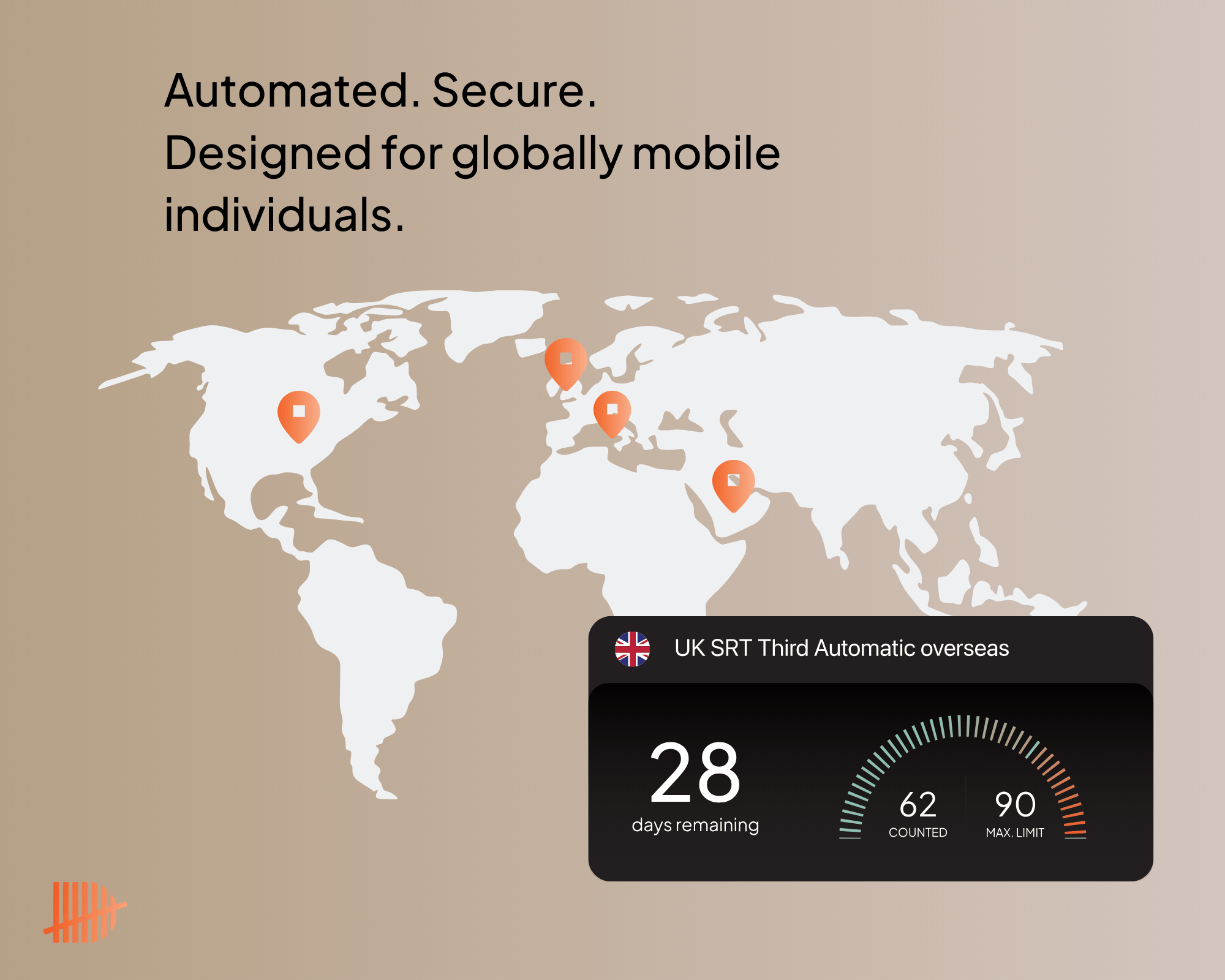

Automated Day Counts

Spreadsheets showcasing day counts are no longer sufficient. The manual methods are prone to unintentional errors and miscalculations. Instead, family offices need systems that:

Automatically log location data in real time.

Show in real-time if family members approach their residency thresholds.

Align records with jurisdiction-specific rulesets.

An automated, real-time view of day counts enables better planning. With tax jurisdiction-specific rules, individuals can trust that day counts take into account the nuances of things like what constitutes as ‘present’ or how exceptional or transit days are dealt with.

Corroborating Evidence

Authorities often dismiss a simple list of day counts. Our case studies show that they are quick to dismiss even simple receipts of purchase, as these don’t sufficiently tell the story of where the person was. Instead, the focus should be on combining day counts with strong supporting evidence, such as:

Boarding passes, itineraries, and entry/exit stamps.

Geo-tagged photos or digital notes from relevant trips.

Meeting minutes or event attendance that align with claimed presence.

Having the evidence documented at the same time and place as day counts creates a substantial body of evidence that leaves authorities with fewer questions and a need for clarification.

Centralised and Secure Files

For the family office, having a centralised place to find this information removes a lot of friction, errors and time-consuming administrative work. A family office should maintain:

Residency packs for each principal: certificates, tie-breaker analyses, logs, and supporting documents.

Entity substance files: board minutes, director presence logs, and local records of control.

CRS/FATCA files: current self-certifications, controlling persons registers, and validation steps.

The goal is to have everything ready to hand in case banks, auditors, or tax authorities request it.

The Daysium Advantage

Daysium was built to make bulletproof residency records achievable. For family offices, our platform:

Automates day counting across jurisdictions, tailored to each family member’s unique tax rules that apply to them.

Creates contemporaneous evidence by pairing location data with geo-tagged documentation.

Generates ready-to-share reports to share with advisors, banks, or tax authorities.

With enquiries and regulatory scrutiny increasing, the difference between a simple log and a defensible residency record could mean millions in avoided tax, faster resolution of disputes, and peace of mind for the family.

FAQ: Tax Residency Records & Family Offices

Why are tax residency records essential for family offices?

Tax residency determines income tax, inheritance tax, and access to treaty benefits. For family offices, poor records can lead to dual-residence disputes, frozen bank accounts due to CRS/FATCA mismatches, and longer, more costly tax investigations.

What mistakes do family offices commonly make with tax residency compliance?

The biggest risks include relying solely on day counts, failing to maintain corroborating evidence (e.g., boarding passes, meeting minutes), and not regularly refreshing residency self-certifications for banks. Even simple receipts or card transactions are often dismissed by authorities as weak evidence.

How does CRS/FATCA reporting affect family offices?

Family offices often manage accounts for trusts, foundations, and family members. Banks are legally required to report tax residency under CRS/FATCA, and discrepancies between reported and actual residency can trigger enquiries, fines, or account freezes.

What kind of evidence do tax authorities accept beyond day counts?

Accepted evidence includes entry/exit stamps, boarding passes, geo-tagged photos, event participation, and signed board minutes. Courts often reject credit card receipts or vague travel records if they don’t prove physical presence.

How can family offices future-proof their residency compliance?

By automating day counts, creating ‘global mobility records’ for each principal, and keeping updated governance and substance records for entities. Working with tax advisors and leveraging technology such as Daysium helps family offices anticipate and defend against audits.

Next Steps for Your Family Office

The regulatory tide in Europe is currently flowing in one direction: toward more data, more scrutiny, and more investigations. For family offices, that means tax residency can no longer be treated as an afterthought.

Globally mobile creatives live across borders — but tax residency rules still count days. In this conversation with Richard Paul, we explore why strong travel records matter more than ever.

Tax residency record-keeping has evolved. For advisors managing globally mobile clients, it is no longer enough to count days and store documents. In a more scrutinised compliance environment, defensibility depends on whether the evidence tells a coherent, contemporaneous story that supports the residency position.

HMRC tax investigations into individuals can be complex, time-consuming and emotionally draining, particularly for high-net-worth and globally mobile individuals. This article explores whether investigations are getting longer, why the wealthy face greater scrutiny, and how strong compliance records and automation can significantly reduce their impact.

Spreadsheet day counting feels familiar, but it often collapses under tax residency enquiries. We examine the hidden risks of spreadsheets and why advisors are increasingly recommending a professional, evidence-led alternative.