The End of the Non-Dom Regime: Insights from Our Partners

24 Nov 2025

The end of the non-dom regime in the UK led to three core themes: increased relocation, UAE as a favoured destination, and behavioural changes around the underlying reasons to leave. Let’s look at what has happened and what you need to know if you’re considering leaving the UK.

The abolition of the UK’s non-dom regime marked one of the most significant shifts in the country’s personal tax landscape in decades. For globally mobile high-net-worth individuals (HNWIs), the change signalled a fundamental realignment of how the UK defines residence, tax exposure, and long-term wealth planning.

In this article, we’ll cover:

What the non-dom regime looked like and what changed

How these changes resulted in 75% of Daysium Partners’ clients having left or actively considering leaving

Relocation and behavioural trends with the UAE, Portugal and Italy among the favoured destinations

What you need to understand before leaving the UK, and why day counting and record-keeping are crucial

Why your next step should be a structured risk assessment of your current position

A Recap of the End of the Non-Dom Regime

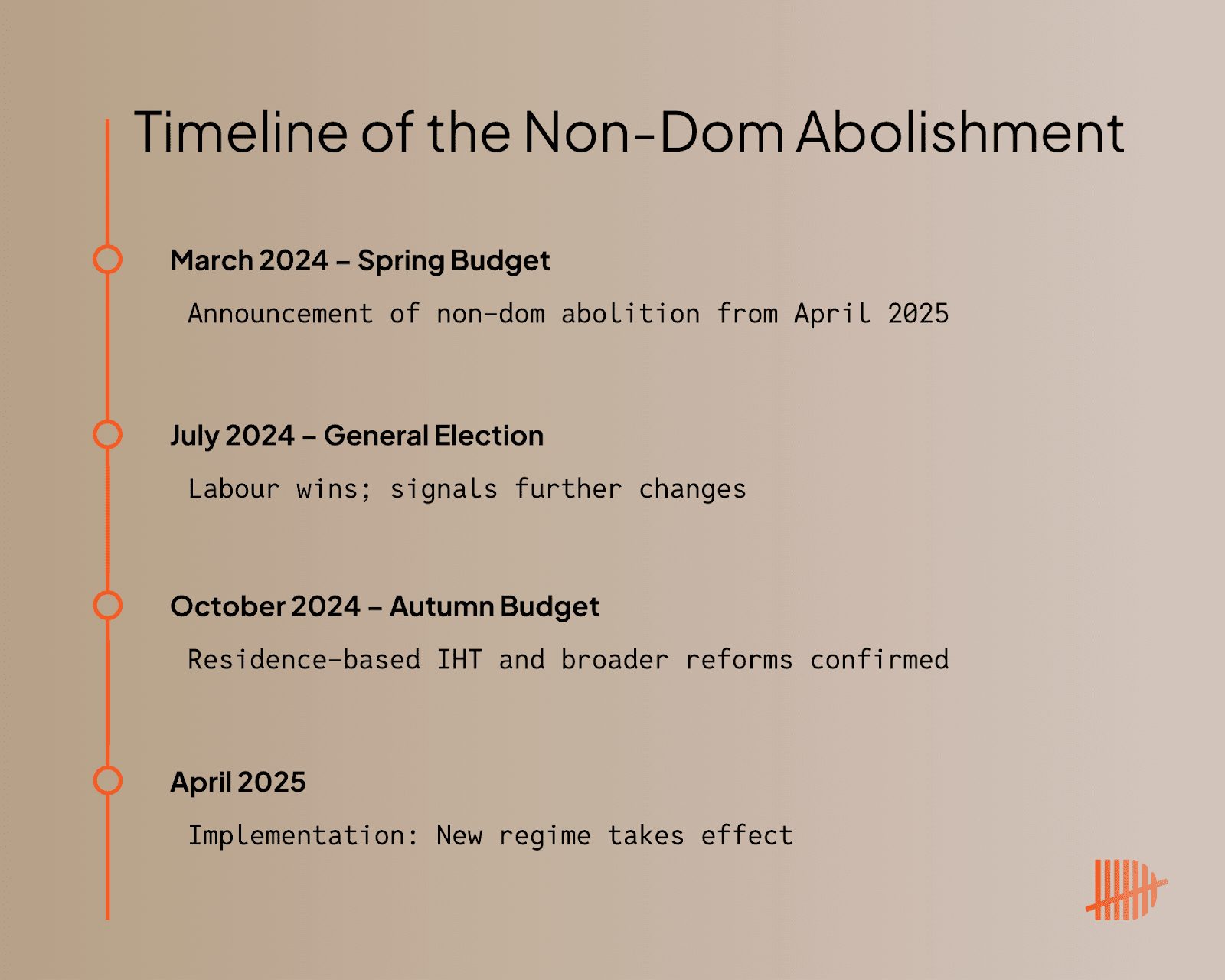

The end of the non-dom regime was brought about by two rapid political steps. First, the Spring Budget 2024 announced that the remittance basis would be abolished from 6 April 2025, replaced with a new residence-based system for qualifying arrivals and returners.

Then, after the general election, the October 2024 Budget expanded the reforms by shifting inheritance tax (IHT) to a residence-based model. This meant that long-term UK residents would eventually bring their non-UK assets into UK IHT regardless of historic domicile. Both governments presented the same rationale: to modernise an antiquated system and remove scope for perceived unfairness.

How the new system works

The new residency-based regime is built around a simple principle: your tax status depends on where you live, not your domicile, with a transitional period for those entering or returning to the UK.

The below chart summarises the main changes:

Old Non-Dom Regime

New Residence-Based System

Basis of Taxation

Determined by domicile status.

Determined by residence.

Foreign Income & Gains

Taxable only when remitted to the UK.

4-year FIG exemption for qualifying new/returning residents; after 4 years, fully taxable.

Eligibility

Non-doms electing the remittance basis.

Must be non-resident for 10 consecutive years before arriving/returning.

Historic Foreign Income & Gains

Could remain untaxed if not remitted.

Temporary Repatriation Facility allows bringing historic FIG to the UK at reduced rates (time-limited).

Inheritance Tax (IHT)

Based on domicile; non-UK assets often excluded.

Based on residence; non-UK assets taxable once UK-resident 10/20 years, with a post-departure tax tail.

Why these changes matter

For many individuals, the end of the non-dom regime is more than a tax shift, representing a fundamental redesign of how the UK views globally mobile wealth. The move to a residence-based IHT system, in particular, had become a significant concern for advisers and clients, creating a clear incentive for some to leave the UK before they become long-term residents under the new rules.

Did the Non-Doms Leave?

Before the formal abolition of the non-dom regime, the consensus among advisers and research houses was that a meaningful number of individuals would exit the UK. For instance, a study by Oxford Economics estimated that between 7% and 32% of non-doms might leave the UK by 2029/30 under specific behavioural-response scenarios.

In practice, the data are still emerging, and it will take some time for the real impact to be unveiled. According to official figures from HM Revenue & Customs, the number of non-domiciled and deemed non-domiciled taxpayers in the tax year ending 2024 stood at approximately 83,000, down marginally (about 1%) year-on-year.

Other analyses have painted a different picture. A report, led by former Treasury economist Chris Walker, suggested that at least 10% of non-doms may have already left the UK in response to the reforms. While a “mass exodus” remains unconfirmed, the expectation of behaviour change and relocation has clearly begun to play out.

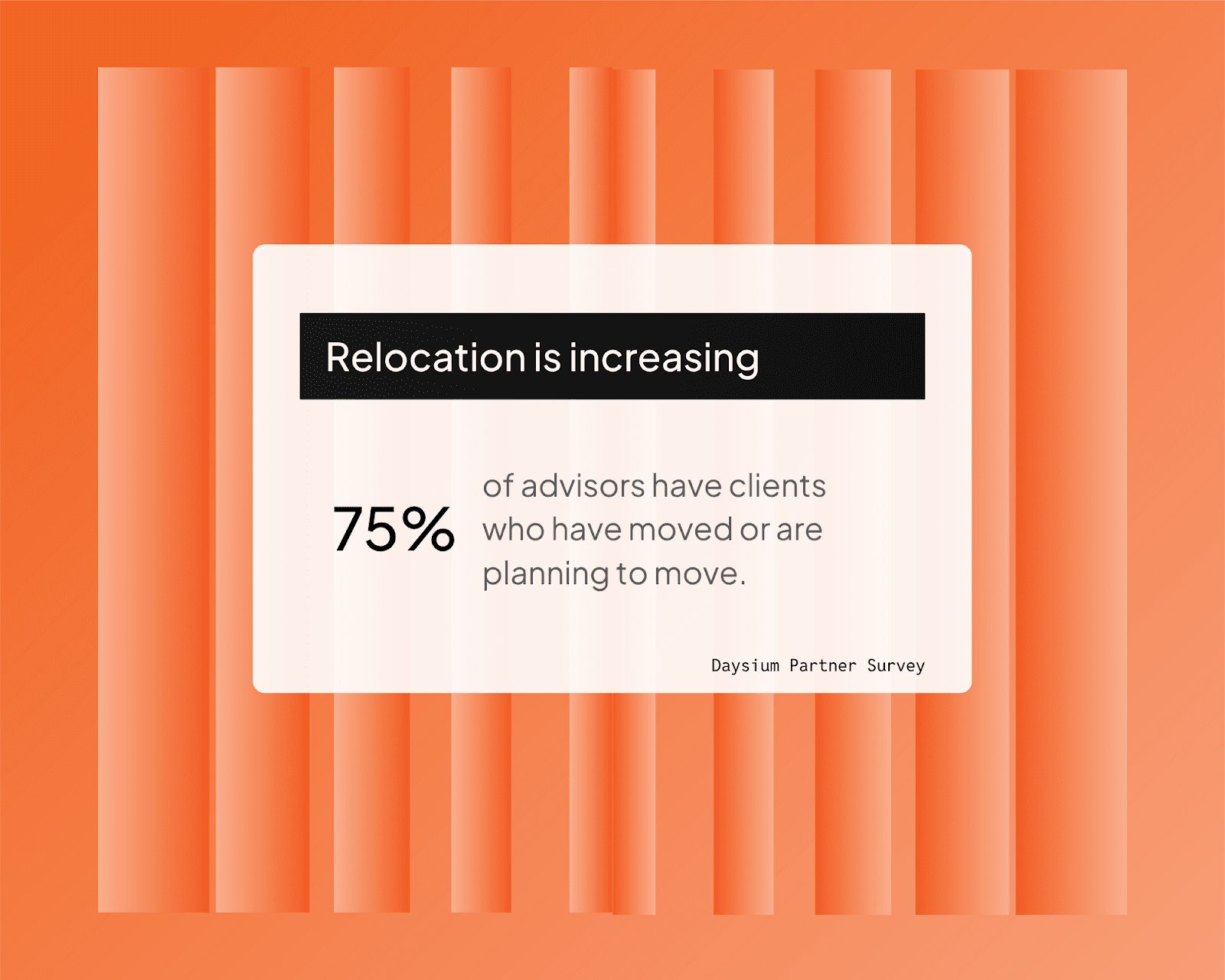

Our Founding Partner Survey confirms this change: 75% of respondents said that clients have either relocated or are actively planning to do so.

Three Themes Emerge as Non-Dom Framework Ends

Our survey points to three main themes that the end of the non-dom regime has brought about.

1. Relocation is increasing and likely to increase

As we just mentioned, most of our partners have clients who have relocated or are actively planning to do so. When asked how competitive the UK now feels for internationally mobile HNWIs:

75% of partners said the UK is less attractive

25% were not sure

Around half of our respondents said they expect somewhat or significantly more clients to leave in the next five years. This suggests that for many HNWIs, the rule change has triggered tangible movement rather than just posturing.

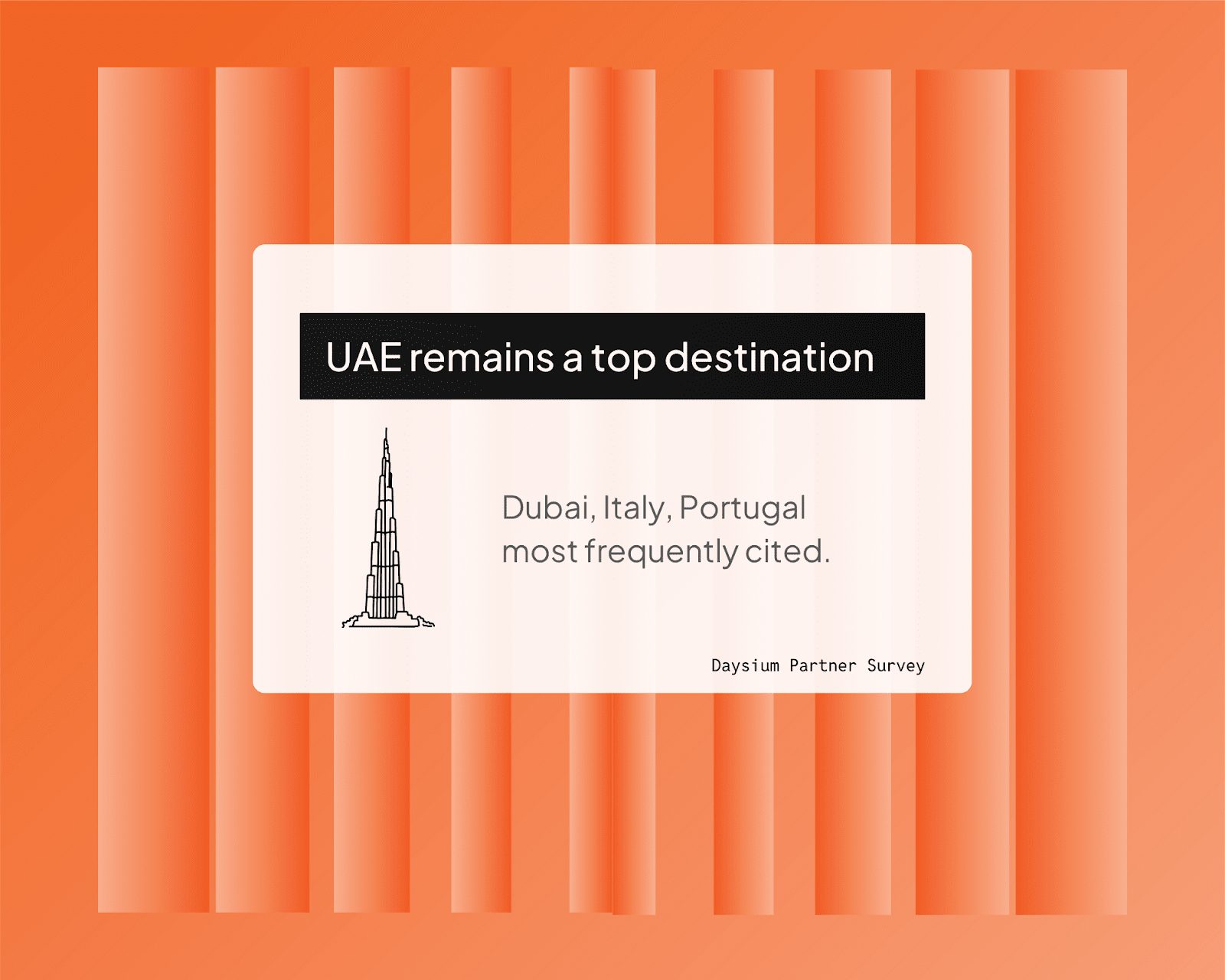

2. The UAE continues to be an attractive relocation hub for HNWIs

For those relocating and considering it, the destinations cited are consistent with global migration flows. At the top of the lists are the UAE (mainly Dubai), Italy, and Portugal. Our partners also mentioned Monaco, Malta, Hong Kong and the Channel Islands as potential relocation hubs.

The appeal is clear: tax-efficient jurisdiction, good connectivity, and a global lifestyle environment. Each jurisdiction offers opportunity, but each comes with its own day-count tests, substance requirements and local reporting, which means relocation planning must be done with both arrival and departure rules in mind.

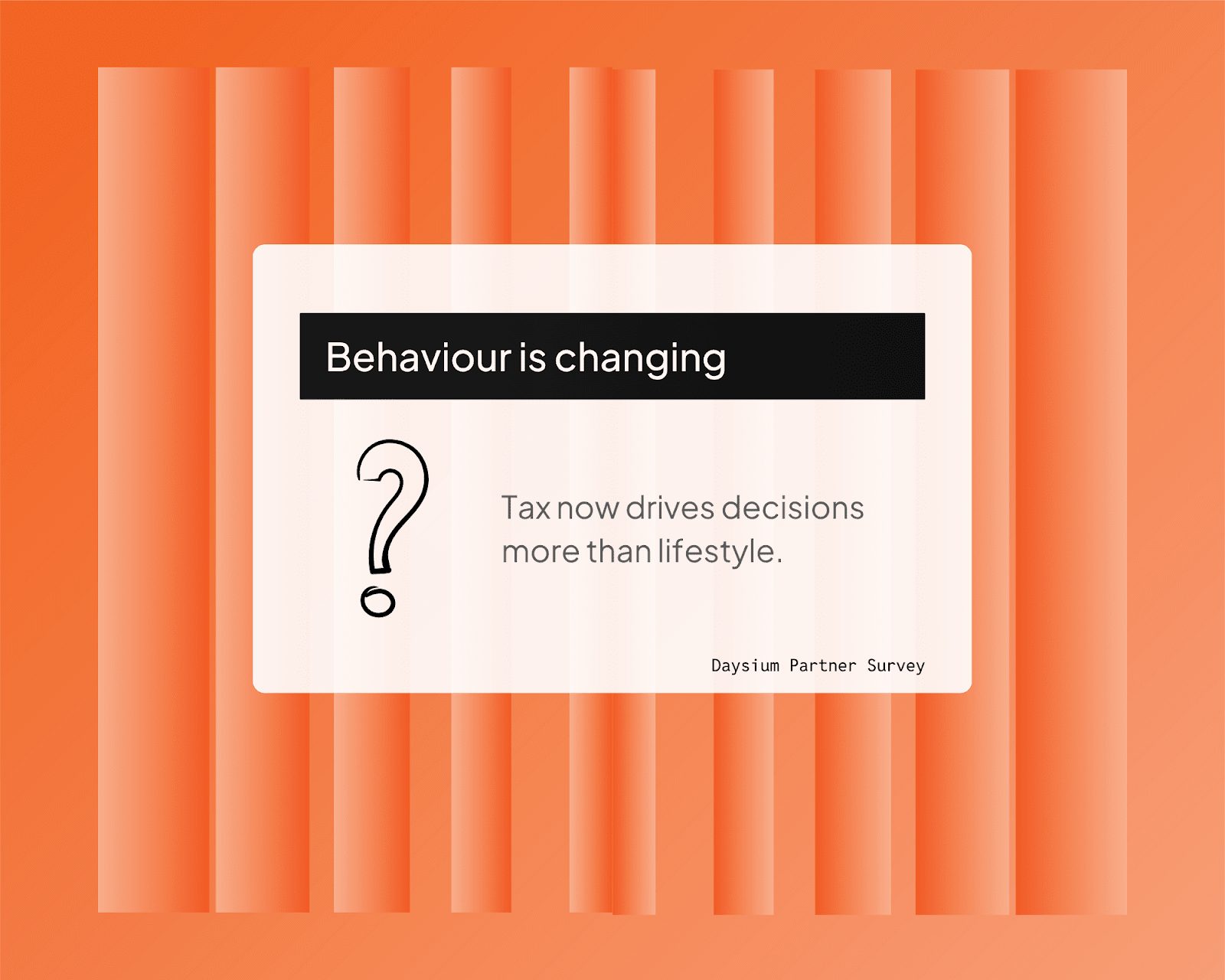

3. Client behaviour has changed – tax now takes a more prominent role.

While lifestyle will always underpin relocation and residence decisions, the survey findings show that tax is now harder to ignore. As one partner put it,

“Tax has become a primary consideration, compared to lifestyle historically.”

It’s not surprising then that partners also reported that clients are increasingly seeking advice. They are curious about the rules, especially those related to Inheritance Tax (IHT), excluding UK investments, or restructuring offshore arrangements.

These findings show that behaviours are changing in response to rules surrounding them. A proactive approach to wealth management, especially around tax residency, is required, no matter whether the decision is to stay or leave.

Are You Considering Leaving the UK?

If you are considering leaving the UK in response to the end of the non-dom regime, there are four key areas to consider.

1. Scrutiny doesn’t end when you relocate

One of the most common misconceptions we encounter in client conversations is the notion that moving abroad closes the UK chapter. In reality:

HMRC can typically raise assessments up to four years after the end of the tax year if an error is made despite reasonable care.

This extends to 6 years where there has been carelessness, and up to 20 years where HMRC believes there has been deliberate behaviour.

For offshore matters or transfers, HMRC has up to 12 years to assess lost tax, even where the behaviour is only careless or reasonable care has been taken.

HMRC’s specialist wealth teams and its Connect data analytics system allow the department to cross-reference flight records, financial data and even social media against declared residence and income patterns.

In some of the tax residency cases we’ve studied, authorities have looked back close to a decade, with outcomes depending on the quality of day-count records and supporting evidence.

2. UK residence on your way out

The Statutory Residence Test (SRT) remains the core framework for determining UK tax residence. Your final year(s) in the UK might involve:

Split-year treatment, where the tax year is divided into a UK-resident part and a non-resident part, depending on when you leave and your work, home and family arrangements.

Day-count thresholds that still apply if you continue to visit regularly, especially if you retain accommodation or close ties here. Day counting, therefore, becomes more nuanced, particularly if you are:

Manning international roles

Sitting on UK boards

Maintaining family property or schooling in the UK

3. New day-count rules where you land

Your destination may have its own flavour of SRT-style rules, minimum presence tests or tie-based thresholds. You’ll need a joined-up view that recognises:

How many days do you need to spend in your new country to become a tax resident there?

How many days can you still safely spend in the UK without re-establishing residence?

Whether any tax treaty tie-breaker rules are likely to be relevant.

This is where an automated system for logging and evidencing days across multiple countries becomes strategically advantageous, rather than just a compliance chore.

4. Getting your evidence house in order

Before you go, and as you settle somewhere else, it’s worth asking:

Can you reconstruct your day count history if HMRC looks back five or ten years?

Do you rely on airline emails and credit card statements, or do you have a structured evidence trail that clearly links you to where you say you were?

Is your advisor able to produce a coherent narrative quickly if an enquiry lands?

We’ve seen how weak evidence (for example, scattered receipts and patchy calendars) can prolong enquiries and create unnecessary risk, even when the final judgment goes in the taxpayer’s favour.

A “Daysium Year” approach – where rules are clearly set, day counts are automatically logged in real time, and evidence is attached to your location history – gives you a defensible narrative, not just a spreadsheet of dates.

FAQ: Common Questions About the End of the Non-Dom Regime

Why did the UK end the non-dom regime?

The UK abolished the non-dom regime to modernise the tax system, remove its domicile framework, and ensure long-term residents are taxed on worldwide income. The government aims to close deemed loopholes and introduce a clearer residence-based system.

How many non-doms have left the UK?

There is no confirmed official total yet, but some early estimates suggest noticeably higher departures than expected. Academic forecasts suggested that only 0.3% would leave. However, some newer analysis indicates that at least 10% of former non-doms may have already relocated or begun the process.

Will there be further changes to the non-dom reforms?

A complete reversal is unlikely, but refinements are possible. The government has signalled openness to adjusting residence-based IHT rules and the Temporary Repatriation Facility. The ongoing debate about competitiveness and investment means targeted tweaks may continue. Still, a return to the remittance-based system is not anticipated.

Does moving abroad end HMRC scrutiny of my affairs?

No. HMRC can still review earlier tax years after you leave and may open or continue enquiries. Time limits can extend up to 12 years for offshore matters, and longer for deliberate behaviour. Accurate day count and evidence records remain essential even after relocation.

Preparing for Your Next Relocation Steps

The end of the UK non-dom regime has created a fundamentally different tax landscape — one defined by the 4-year FIG window, a new residence-based IHT system, increased relocation activity, and sharper investigatory focus from HMRC. In this environment, day counting is no longer a background administrative task but a strategic part of tax planning. For anyone with international mobility, defensible digital records are now essential, especially as authorities gain greater access to cross-border data.

Whether you plan to remain in the UK or relocate, the most critical first step is understanding your personal exposure. Our Tax Residence Risk Score assessment is designed to help you do exactly that. Built with input from the UK’s Contentious Tax Group, it evaluates your likelihood of investigation, the strength of your day count and evidence trail, and the practical steps you can take to reduce risk before making significant decisions.

Take the assessment, review your personalised risk profile, and share the results with your advisor to build a calm, data-driven plan for your next move.

Discover how to be tax compliant with Daysium

Created in partnership with industry experts, tackle the complex challenges of day counting and tax record-keeping.

As an HNWI and globally mobile individual, you’re likely to come across HMRC nudge letters. But what are they, why they’re sent, who might receive one, and what are the practical steps to take with a tax advisor to prevent escalation?

HMRC tax investigations into individuals can be complex, time-consuming and emotionally draining, particularly for high-net-worth and globally mobile individuals. This article explores whether investigations are getting longer, why the wealthy face greater scrutiny, and how strong compliance records and automation can significantly reduce their impact.

Location data in tax audits can protect HNWIs. As global tax authorities ramp up AI-driven investigations, even minor discrepancies in day counting can lead to major liabilities. This article explores real court cases and how platforms like Daysium help individuals stay compliant, confident, and audit-ready.

Flying private gives you discretion, but not invisibility. Every private jet flight creates travel records that can be requested during tax enquiries. This article explains what gets recorded, where the gaps lie, and how to proactively protect your tax residency status with robust, digital evidence using compliance tools.