Relocating Abroad? Key Tax Considerations to Avoid Costly Mistakes

03 Mar 2025

Thinking about moving abroad? Understanding tax considerations when relocating is essential to avoid unexpected tax liabilities. From exit taxes to residency rules, this guide covers key areas to review before your move.

Thinking about moving countries? While it’s an exciting move, understanding the tax considerations when relocating abroad is crucial to avoid unexpected costs. Many globally mobile individuals assume that leaving a country means leaving its tax system. However, that’s not always the case.

Without proper tax planning, exit taxes, double taxation, and ongoing obligations can create financial headaches down the line. While tax laws differ across jurisdictions, here are some general considerations that individuals relocating abroad should consider.

Please remember to always discuss your specific tax circumstances with a professional tax advisor.

Tax Considerations When Relocating Abroad

Every country has different rules on tax residency, exit taxation, and ongoing tax obligations. A few key areas to be aware of include:

Ongoing Tax Obligations

Leaving a country doesn’t necessarily mean leaving its tax system. Some governments continue to tax former residents under certain conditions.

The U.S. taxes its citizens on worldwide income, regardless of where they live.

The UK applies a split-year treatment that might apply when moving in or out of the UK during a tax year.

Exit Taxes

Some countries impose exit taxes on individuals moving to other countries. This is often applied to unrealised capital gains when residents leave.

💡For example, France, Canada, and the U.S. apply capital gains tax upon departure in certain situations.

When relocating assets, understand how these are taxed by the country you’re moving them away from. This can help structure assets more strategically during relocation.

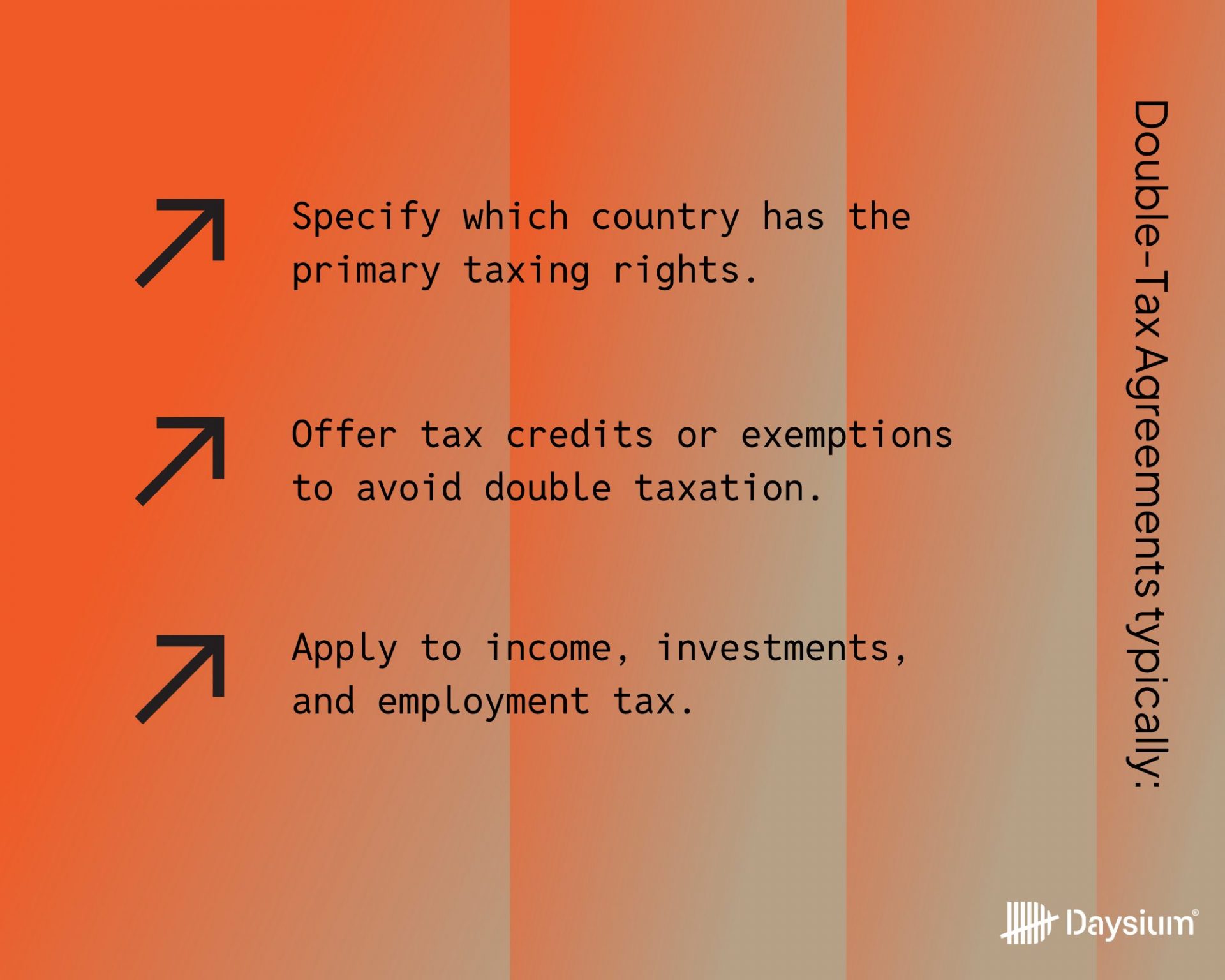

Double Taxation & Tax Treaties

Individuals relocating abroad could face taxation in both their home and new country. Many jurisdictions have Double Taxation Agreements (DTAs) in place to prevent this. However, their scope and application may vary from country to country.

Reporting Requirements

Even after relocation, some governments require continued tax reporting. You may need to report to your previous tax jurisdiction and stay aware of potential tax liabilities.

💡Many countries have agreements for automatic exchange of financial information, which means that even if you don’t report directly, your financial information may still be shared between tax authorities.

If you need to monitor things like day counts to avoid risking tax residency, you should consider using automated day counting tools like Daysium. These can help maintain accurate records and help you plan future travels without risking non-compliance.

How to Determine Your Tax Residency When Moving Abroad

Tax residency rules differ across countries and depend on various factors. Your tax residency can be determined by the time you spend in a particular jurisdiction and the economic ties you have. These factors may be considered on their own or together.

For example, you may have to meet a specific day count together with sufficient economic ties to be considered a tax resident. Alternatively, it may be enough in some jurisdictions to meet the day counting threshold. You can read some more about tax residency in our previous article.

When relocating, you need to understand your new country’s tax residency requirements and the rules in tax jurisdictions you frequently visit. Having a clear and updated view of your day counts helps you avoid accidental tax residency triggers.

Core Tax Planning Areas to Review

When planning an international move, different tax areas may need attention, including:

Income Tax: Will earnings be taxed in the new country or remain subject to taxation elsewhere?

Inheritance Tax: Does the move require adjustments to estate planning?

Capital Gains Tax (CGT): Would selling assets before relocation be more tax-efficient?

Investment & Wealth Structures: Are offshore holdings aligned with the new tax environment?

Mapping your finances and assets can help untangle the potential tax considerations. Speaking with an accountant or advisor specialising in expat taxation can help ensure you don’t miss out on beneficial strategies.

Why Keeping Tax Records Matters When Moving Countries

Global tax authorities are increasingly leveraging AI and data analytics to identify non-compliance. Authorities are scrutinising the affairs of the wealthy, especially when individuals are moving countries. Tax laws are intricate and complex, so the risk of accidental non-compliance is high.

Maintaining clear records can be crucial in the event of a tax inquiry. Proactive planning is vital in record-keeping. Even if you aren’t sure you’ll be moving countries, generating and keeping records can make the potential move easier.

Digital tools like Daysium allow individuals to log travel days, store supporting documents, and generate compliance reports, helping to create a robust record trail. You won’t just have records from the immediate time of your relocation but can create a compliance trail before and after the move. If the authorities ask for your records, you can simply state, “There’s nothing to see here, everything is in order.”

Seeking Expert Guidance

International tax rules can be complex, and professional guidance can help individuals navigate tax considerations when relocating. As Paul Aplin OBE, Daysium Senior Advisor, recently wrote,

My advice to anyone who does not hold a tax qualification – no matter how well they think they know the subject – is always to check their understanding with someone who is qualified.”

Paul Aplin OBE, Daysium Senior Advisor

Seeking professional guidance is essential because, as Paul writes, it can “ensure that the outcome being sought is the one that will actually transpire: some actions cannot be undone.”

Engage with tax professionals as soon as you consider a move. Our Partner network can help you find expert advice in different tax jurisdictions. You’ll gain more clarity on available options and the potential tax considerations that can impact when or where you want to move.

Assessing Tax Exposure Before Moving

Not sure about potential tax liabilities? A structured risk assessment can help identify areas of concern and ensure individuals are prepared.

Understand potential tax obligations.

Identify reporting requirements.

Ensure readiness for compliance checks.

We’ve developed a quick risk assessment in partnership with the UK’s Contentious Tax Group. The assessment helps you explore your current tax residency risk score with actionable steps to improve your situation. You can use it to explore your situation before or during a relocation.

Relocating abroad is more than just a logistical move. It requires careful financial and tax planning. While tax laws vary by country, being proactive about tax residency management can help minimise risks and ensure compliance.

With tools like Daysium, individuals can automate their day counting and compliance. Our platform makes it easy to attach supporting evidence to your records, strengthening your compliance position. With our network of tax experts at your reach, you can get the advice to guarantee strategic planning. You don’t need to worry about the tax considerations when relocating abroad; instead, you can focus on preparing for the adventure of changing countries.

When tax residency plans change, the risks are not always obvious. With insight from Scott Homewood at Trident Tax, we explore what families should consider when leaving the UAE and reassessing their position.

Relocating to the Crown Dependencies can feel like a fresh start, but day counting and tax residency rules often mean you need to remember your past. This article explores why UK days still matter, how residency rules differ across Jersey, Guernsey and the Isle of Man, and what HNWIs should prepare before and after a move.

European programmes are tightening or closing, non-EU hubs like the UAE and Saudi Arabia are rising, and tax authorities are paying closer attention to how and where globally mobile individuals spend their time. For HNWIs, success now depends on strategic planning, accurate day counting, and defensible residency records, not just qualifying investment.

Visiting family in Europe can blur the lines of Schengen compliance. Many HNWIs assume family connections offer more travel freedom, but the 90/180-day rule may still apply. This article explains the nuances of the Schengen rule for family travel and how Daysium helps you stay compliant and confident wherever you go.