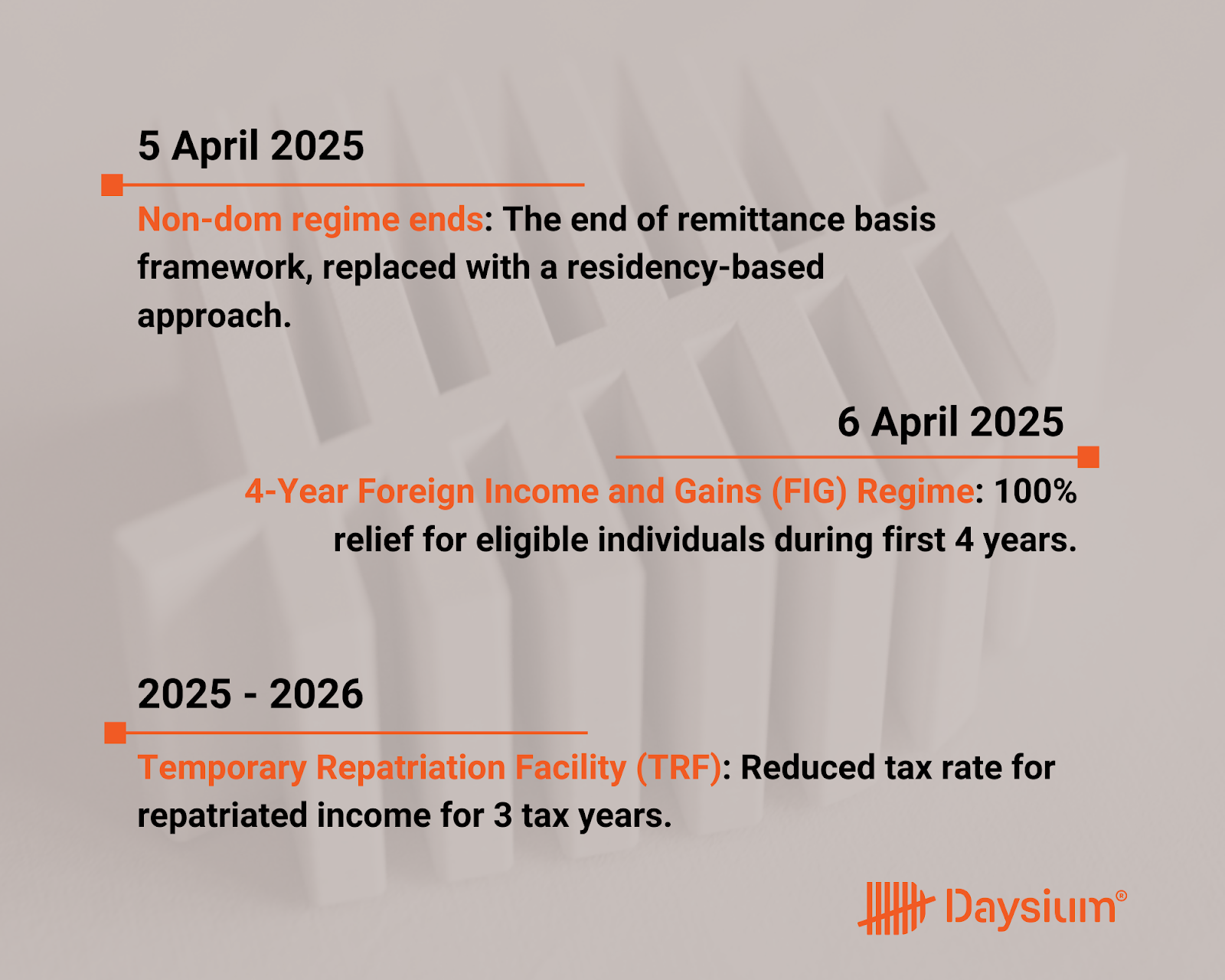

The UK Budget introduced several pivotal changes for tax and residency rules. These included increasing Capital Gains Tax (CGT) and changing Inheritance Taxation (IHT) framework. It also moved forward with the previously set plans to scrap the non-dom regime. The UK Government is looking to replace it with a residency-based system.

Here are the critical details:

A 4-year FIG Regime

The introduction of a new 4-year foreign income and gains (FIG) regime will be available for new arrivals to the UK for their first four years of tax residency, provided they haven’t been UK tax residents in the 10 consecutive years before their arrival. The regime provides 100% relief on eligible FIG for those four years.

Furthermore:

-

- From April 6 2025, all former remittance basis users ineligible for the 4-year FIG regime pay tax at the same rate as other UK residents on any newly arising FIG.

-

- Former remittance basis users continue to pay tax on FIG, which arose before April 6, 2025, when they remit to the UK.

-

- If someone leaves the UK temporarily during the 4-year FIG period, they can still claim the FIG relief when they return, as long as it’s within the 4-year timeframe.

For example, if an individual leaves the UK in years 2 and 3 and returns in year 4, they remain eligible for FIG relief in that fourth year. However, they can’t claim it in year 5 since it falls outside the initial 4-year period, which is only valid for up to 10 consecutive years.

Trusts

No Tax Protection: Non-domiciled individuals who don’t qualify for the 4-year FIG relief won’t be protected from tax on FIG within their trusts.

Protected Trusts: FIG from protected non-resident trusts won’t be taxed unless paid to UK residents who don’t qualify for the 4-year FIG relief.

Taxable Distributions: FIG from these trusts may be taxed on UK resident settlers or beneficiaries without 4-year FIG relief if matched to distributions they receive from the trust globally.

A Temporary Repatriation Facility (TRF)

The TRF allows individuals previously taxed under the remittance basis to bring in certain untaxed foreign income and gains (FIG) from before 2025 at a reduced tax rate over a three-year period:

-

- 12% tax rate for the first two tax years.

-

- 15% tax rate for the final tax year.

For individuals benefiting from offshore trusts, the TRF applies if they used the remittance basis and the funds are linked to pre-2025 gains within the trust. Those who pay TRF tax can choose to remit these funds later, beyond the TRF period.

Inheritance Tax

The UK is introducing a residency-based inheritance tax (IHT) system that affects how non-UK assets are taxed.

-

- Residency Requirement: Non-UK assets will be subject to IHT if the individual has lived in the UK for at least 10 out of the last 20 tax years before the taxable event (like a death). However, if they lived in the UK for only 10–19 years, the period their assets stay subject to UK inheritance tax after they leave the UK will be shorter.

-

- Asset Exclusion: Non-UK assets in trusts won’t automatically be excluded from IHT. Assets are only excluded when the person who placed them in the trust (the settlor) is not a long-term UK resident. If the settlor is a long-term resident, the assets will be subject to IHT.