Manual vs Automated Day Counting: What Family Offices Should Know About Residency Risk

12 May 2025

For family offices managing globally mobile clients, tax residency is a strategic part of wealth management. But reliance on manual day counting leaves many exposed to risks that an automated day counting platform can solve. This article looks at how automation enhances compliance, reduces audit exposure, and brings clarity across jurisdictions.

For family offices managing the affairs of internationally mobile individuals, tax residency is more than a line item. It’s a strategic risk area. Whether advising on relocation, managing structures, or preparing for audits, day counting sits at the heart of compliance.

Yet many offices still rely on fragmented, manual tracking methods to manage this critical data point. In this post, we explore the realities of manual versus automated day counting and how family offices can move toward more defensible, scalable solutions while ensuring their clients remain compliant in an increasingly data-driven tax environment.

This scrutiny falls disproportionately on high-net-worth individuals (HNWIs) with complex international footprints. For family offices, the implications are clear: day count accuracy is now a cornerstone of effective governance and reputational protection.

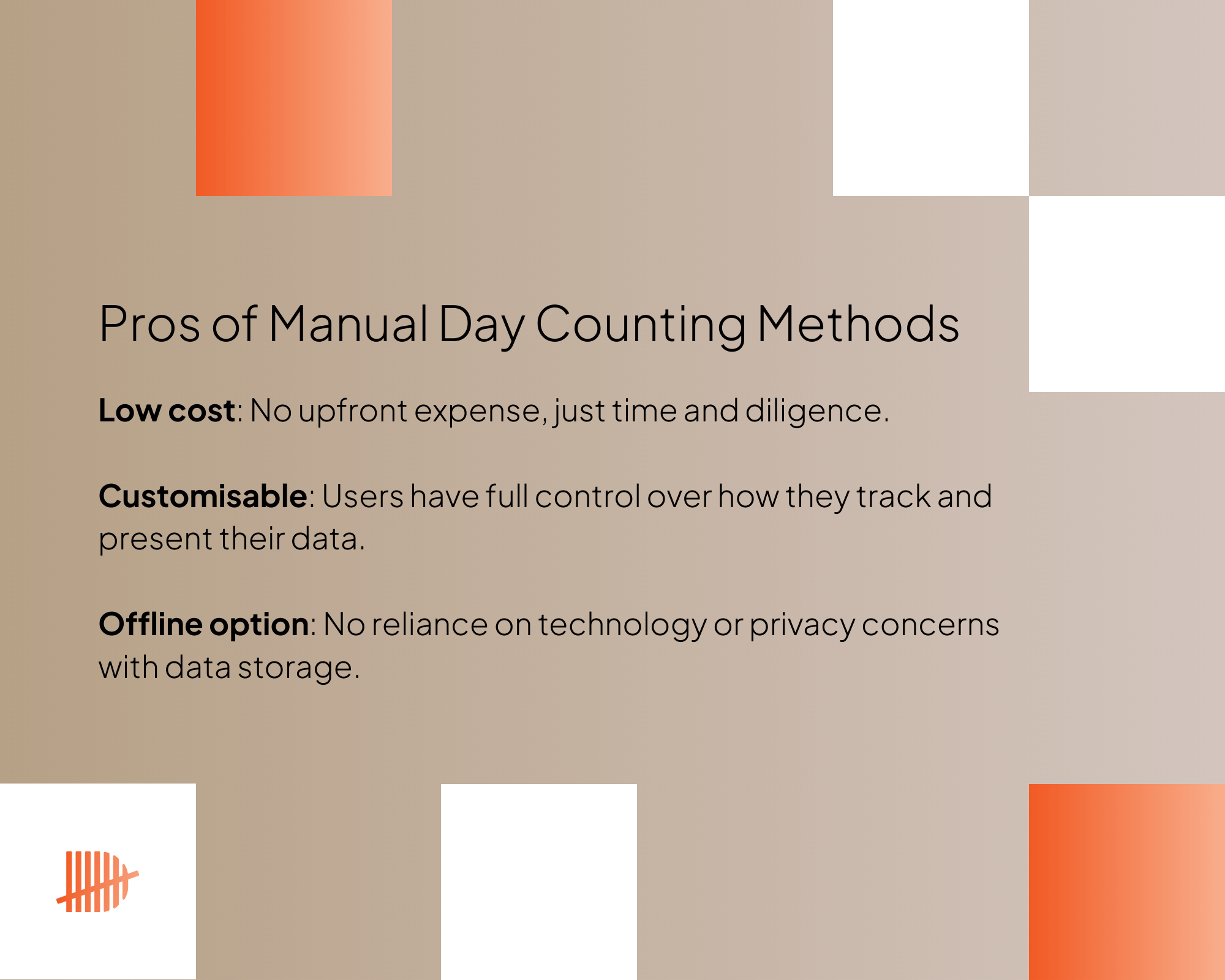

Manual Day Counting: Still Common, Increasingly Risky

Spreadsheets, calendars, saved flight emails; these manual methods remain prevalent. They’re familiar and low-cost, but they introduce significant compliance and operational risks when applied to modern family structures.

Common Manual Methods

Spreadsheets: Users input dates and jurisdictions, often supported by notes or receipts.

Travel calendars or diaries: Some record entries and exits on paper or in digital calendars.

Email and flight confirmation receipts: Others search inboxes to reconstruct past travel, though this is far less effective when flying private, where there may be no boarding passes or standard booking confirmations.

Compliance Risks for Family Offices

While manual day counting methods may seem manageable at first, they introduce hidden risks that can escalate quickly, especially when managing multiple principals or navigating cross-border complexity. For family offices tasked with safeguarding both compliance and reputation, these are the most pressing concerns:

Inconsistency Across Principals

Different individuals (and advisors) use other methods, creating governance challenges and errors. Dates get missed, misremembered, or logged inconsistently, especially over a busy year.

Weak Audit Trail

Without contemporaneous evidence, manual records are often insufficient in the eyes of tax authorities. Credit card receipts and car rental confirmations aren’t enough. As our previous case study into an Irish tribunal put it, a purchase proves nothing but the purchase. It can’t show your physical presence in a specific location convincingly. No Real-Time Visibility

There is no proactive warning system when someone is approaching a residency threshold, whether for tax, immigration, or tie-breaker rule concerns.

Staff Hours Lost to Verification

During audits or annual reviews, staff spend valuable time piecing together fragmented records.

Day Counting at Scale: Why Manual Fails in Multi-Client Environments

When managing more than one individual or household, the burden of manual methods grows exponentially.

Children attending school in one jurisdiction while parents reside elsewhere.

Principals and spouses with different travel habits.

Non-resident directors with recurring UK presence.

Family members considering second citizenship or tax-friendly relocation.

Each scenario carries potential tax implications that hinge on day counts. A manual system cannot deliver the clarity and consistency needed to manage this risk at scale.

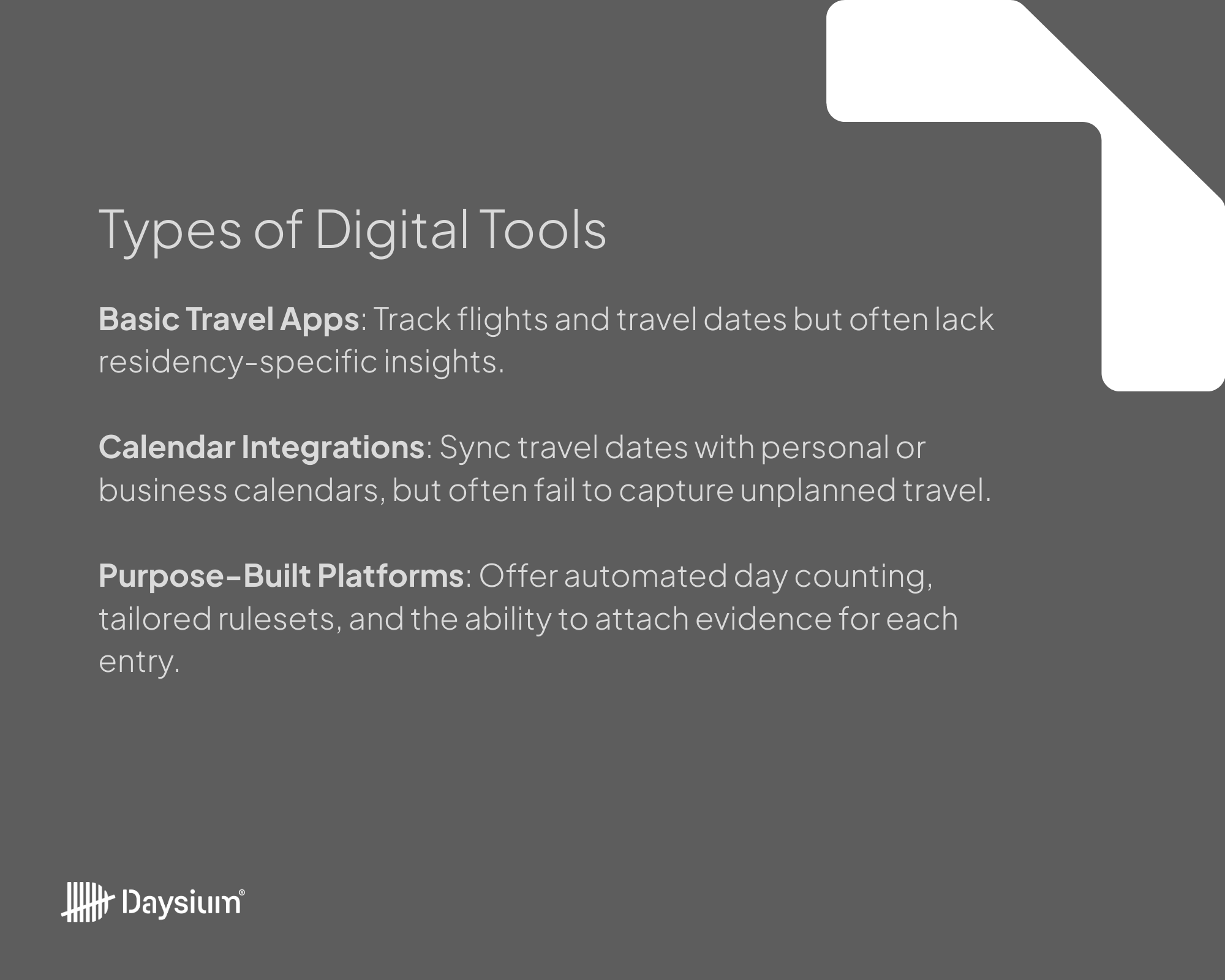

Automated Day Counting: A Strategic Upgrade for Modern Compliance

Digital transformation is reshaping compliance and automated day counting platforms are now essential for family offices managing internationally mobile clients.

What the Best Platforms Offer

When evaluating a day counting platform for tax residency, not all tools are created equal. Family offices should look for systems that go beyond simple travel tracking. They want to look for tools offering precision, legal defensibility, and scalability tailored to the complexities of global clients. Here’s what leading platforms bring to the table:

Real-time day counting via GPS and movement data

Tailored tax rulesets aligned to jurisdiction-specific thresholds (e.g., UK Statutory Residence Test)

Contemporaneous evidence, including geo-tagged images, receipts, and event notes

Audit-ready reporting exportable for use in inquiries or legal reviews

Strategic Benefits for Family Offices

By implementing the right platform, family offices can future-proof their residency oversight processes and reduce the burden of manual compliance:

Reduced Risk Exposure

Automation minimises human error and ensures day counts are supported by location and evidence data.

Efficient Internal Governance

Centralised platforms streamline oversight, improving collaboration between family office teams, legal counsel, and external tax advisors.

Preparedness for Audit or Inquiry

Inquiries are often retrospective. Automated platforms build a defensible record from day one, not after the fact.

FAQ: What Family Offices Ask About Day Counting

1. Why isn’t a spreadsheet sufficient for day counting?

Spreadsheets can track dates but lack tax logic and offer no evidence. They’re rarely enough in the event of an audit, especially when challenged across multiple jurisdictions.

2. What evidence do we need alongside day counts?

Geo-tagged photos, boarding passes, transaction logs, and location metadata. Tax authorities increasingly expect contemporaneous proof that confirms physical presence.

3. Are all day counting apps suitable for compliance?

No. Many apps track travel for expenses or diaries. For tax residency, the app must align with tax-specific thresholds and support evidence collection.

4. How do automated platforms know which days count toward residency?

Advanced day counting platforms use location data combined with jurisdiction-specific rules (such as HMRC’s SRT) that are coded into the app.

5. What if a client only needs records retrospectively?

Platforms like Daysium allow for retroactive input but automated logging from the start reduces the future administrative burden significantly.

Final Thoughts

Residency isn’t just a tax checkbox. It’s a reputational and financial risk area that demands precision. For family offices tasked with protecting the interests of global clients, automated day counting platforms provide a structured, scalable solution. They reduce the risk of inquiry, improve internal oversight, and offer a clearer picture of compliance across time.

The era of relying on memory and scattered logs is over. In the face of a changing regulatory climate, real-time compliance is strategic compliance.

Tax residency record-keeping has evolved. For advisors managing globally mobile clients, it is no longer enough to count days and store documents. In a more scrutinised compliance environment, defensibility depends on whether the evidence tells a coherent, contemporaneous story that supports the residency position.

As an HNWI and globally mobile individual, you’re likely to come across HMRC nudge letters. But what are they, why they’re sent, who might receive one, and what are the practical steps to take with a tax advisor to prevent escalation?

Relocating to the Crown Dependencies can feel like a fresh start, but day counting and tax residency rules often mean you need to remember your past. This article explores why UK days still matter, how residency rules differ across Jersey, Guernsey and the Isle of Man, and what HNWIs should prepare before and after a move.

Spreadsheet day counting feels familiar, but it often collapses under tax residency enquiries. We examine the hidden risks of spreadsheets and why advisors are increasingly recommending a professional, evidence-led alternative.