Navigating the complexities of tax compliance is an intricate act in a world rich with data. Paul Aplin OBE, a renowned tax writer and Senior Advisor to Daysium, shares his insights into the significance of these data trails. Sit back and venture with us into a world where a simple card transaction has the potential to impact the course of a tax investigation.

The Data Wake

In his book Apollo 13, US astronaut Jim Lovell shares the story of a night flight from an aircraft carrier. A shorted electrical circuit left every bulb on his instrument panel dead. There was no moon and clouds obscured the stars. Where was the ship? Lovell’s options were unenviable, but as his eyes adjusted to the dark, he saw a faint greenish glow in the sea below him. It was a trail of phosphorescent algae, made luminous by the carrier’s propellors. It rendered the ship’s wake visible in the darkness and guided him all the way back to the flight deck.

In the same way, in this data-driven world we now inhabit, most of us navigate by and leave behind us trails of data. Some of these trails are obvious, and we leave or follow them consciously, such as with social media; others we leave largely unconsciously, but either way, they reveal things about our whereabouts, interests and lifestyles that are of great interest to businesses we buy goods and services from and, on occasions, to tax authorities. The patterns and details hidden in the data can yield critical insights.

A tax official from one European country showed me how data drawn from sets of business accounts could be visualised using scatter-diagrams for specific figures across thousands of similar enterprises. He was not interested in the large blob of results in the centre of the screen but in the outliers: why were they so different? The figures might not stand out on their own, but in the context of a vast sea of results, they did so very clearly. They indicated the existence of a trail worth following: they were candidates for investigation.

Modern bookkeeping and accounting software can capture details from invoices, receipts and other documents and store vast amounts of information. A friend who specialises in data analytics recently showed me how he would look for things that might be of interest to a tax authority in a set of business records using data analytics software. “Let’s look for some private expenditure that has been put through the business,” he said, “say restaurant bills.” There were hundreds, all of which might perfectly reasonably have been claimed as business expenses, but just as I was thinking that, he narrowed the search to weekends and then ran a second search on hotel bills with matching dates and double occupancy. In two or three minutes, he had enough to justify asking some potentially embarrassing questions. He had found detailed information about personal behaviour, right down to what had been ordered on room service one hot summer night.

As individuals, we leave a data trail of where we were, when, where we shopped and even what we bought. In the context of tax residence, such data can be extremely valuable in proving that a taxpayer was or was not resident in a particular jurisdiction. In one UK case, the use of a bank card at a petrol station was taken as evidence of the cardholder’s location at that point in time. The tax consequences of being a resident or non-resident can be huge, and I have known situations where that question hung on being able to prove where the individual was on one particular day.

Personally, I don’t view this negatively: if you have nothing to hide, then data trails may just provide the evidence you need to prove your point. If you have something specific that you need to prove, then there is no substitute for robust evidence gathered and stored securely at the time of the event or transaction. You do, however, need to avoid inadvertently leaving false trails: think twice, for example, before lending a loyalty card or bank card to someone (and before you say, “no-one would do that”; trust me, it happens).

Data wakes and shrewd data analytics can catch out the unwary, but if understood and properly used, they can equally represent the route to safety.

The data you leave behind in today’s data-driven world can tell powerful stories. Your ability to navigate this data richness is critical, especially in the realm of tax residency. If you’d like to strengthen your tax compliance and generate robust, contemporaneous evidence to support your tax residency claims, join the Daysium waitlist now.

Strategic Compliance: Leveraging Daysium in the UK’s New Non-Dom Tax Era

Significant changes are coming to the UK tax system for non-UK domiciled individuals (non-dom) with the introduction of the Spring Budget 2024, effective April 2025. The transition requires careful navigation and day counting could become increasingly vital to ensure full tax compliance.

During this transition, the Daysium platform can provide a critical tool for individuals and tax advisory teams, offering precise day-counting and secure record-keeping. In this article, we’ll discuss the upcoming legislative changes, their potential consequences and illustrate how Daysium can enhance tax compliance.

How Are UK Non-Dom Rules Changing?

The UK Government announced in the Spring Budget 2024 that it would be introducing a new residence-based system to replace the current remittance basis of taxation for non-doms. The new system is summarised in the below table:

Who?

New arrivals who haven’t been UK residents for 10 consecutive years.

Existing tax residents who’ve been tax residents for fewer than four years are eligible for the non-dom regime.

Existing tax residents who’ve been residents for more than four years.

Taxation under the new system:

Full tax relief for the 4-year period of subsequent UK tax residence on their foreign income or gains (FIG) arising during this period.

Full non-dom relief until the end of their 4th year of tax residence in the UK.

Any newly arising FIG is fully taxed in the UK, regardless of domicile.

There will be transitional arrangements for existing non-doms. These include a temporary 50% reduction in FIG subject to tax in 2025/26 for those who will lose access to the remittance basis on 6 April 2025 and aren’t eligible for the new exemption regime. There will also be protections in cases where FIG arose in protected non-resident trusts before 6 April 2025. FIG from these will not be taxed unless distributions or benefits are paid to UK residents who’ve been here for more than four years.

The discussion around the UK non-dom regime has been ongoing for years. The Conservative government’s decision to abolish it came as a shock, while not necessarily a surprise, to many.

More Changes in the Horizon?

However, the above changes could be just a start for the non-dom regime. Current UK Prime Minister, Rishi Sunak, announced that there will be a General Election on 4 July 2024. The Conservative Government that proposed the changes may not be in power when the changes are to come into effect and the Labour Party has already announced it may push ahead with further changes.

Labour has indicated that it would include all foreign assets held in a trust within the scope of UK IHT whenever they were settled and remove the proposed temporary 50% reduction from foreign income subject to UK tax in 2025/26.

The party has also indicated that it would consider the investment incentive available to individuals eligible for the new four-year regime to ensure UK investment income is free of tax, potentially scrapping it altogether.

Potential Impact of the Changes on HNWIs

The impact on individuals and families largely depends on how long they’ve been domiciled in the UK. However, there will be increased tax liabilities and compliance complexities involved for almost everyone currently operating under the system. Residency status could have an increasingly important role to play in a few ways.

Let’s consider that an individual leaves the UK temporarily during the proposed four-year period. They can make a claim under the regime for any qualifying tax years remaining on their return to the UK.

However, this will not apply to anyone who was resident in the UK in the 2023/24 tax year and returns to establish UK tax residence from 6 April 2025 or later. The exception is those who were not resident in the UK for ten UK tax years before their return.

It’s also worth noting that anyone arriving in the UK from 6 April 2025 who hasn’t been resident outside of the UK for at least ten UK tax years will no longer be eligible for certain tax benefits. These include oversees workday relief and the broader benefits of the FIG regime.

How Have HNWIs Responded?

Research funded by the Economic and Social Research Council (ESRC) suggests that scrapping the regime would have only a modest impact on UK non-doms. Their research shows that only 0.3% of non-doms would leave the UK — just 77 people. That research points to previous UK reforms in 2017 that restricted access to the regime. Then, around 0.2% of long-staying non-doms and around 2% of non-doms that had arrived in the UK less than three years ago left.

However, there is much pushback against this view. In a Guardian article published in April after the announcement, many advisors to wealthy individuals said their clients aren’t just thinking about leaving but are actively looking for alternatives.

Nimesh Shah, the chief executive of Blick Rothenberg, told the newspaper,

“I’ve got people who only moved to the UK recently, and have built their lives and businesses here and have their children in schools here. But from next April they will be exposed to worldwide taxation. It is a cliff edge; it’s not surprising that they are looking at leaving.”

Where Are Non-doms Headed?

Non-doms don’t have to move out of Europe to benefit from more beneficial systems. While European countries have been tweaking the so-called golden visa frameworks in recent years, there are still options available to provide strategic alternatives to wealthy clients.

These include countries like Italy, which offers a ‘flat tax’ of €100,000 (~£85,200) available, irrespective of their earnings. France, Greece, Cyprus, Malta, Portugal, and Spain are other options many consider, along with locations with low or non-existent income taxation. These include places like Monaco and, a bit further afield, Dubai.

Introducing Daysium: A strategic Tool for Compliance

If the changes are to go ahead, residency status and day counting will become increasingly crucial for globally mobile individuals. Whether a client is considering a move to the UK or is looking to relocate, having accurate data on day counting will be vital. Recent years have shown that HMRC is also increasingly focused on investigating the tax affairs of the wealthy to bolster its tax coffers.

Daysium offers a powerful tool for any current non-doms in the UK. It can also help those who relocate out of the UK and retain close ties to the country.

Tailored Tax Rulesets

Daysium leverages artificial intelligence to create precise tax Rulesets tailored to individual day-counting needs. Our Clients select applicable Rulesets upon joining, adhering to the advice provided by their financial or tax advisors. Importantly, these Rulesets can be adjusted to accommodate changes in a Client’s situation, an essential feature for globally mobile individuals facing evolving tax regulations.

Automated Day Counting

Daysium automatically calculates each client’s day count using GPS and movement data from their phone, ensuring accuracy and reliability. Clients can review and modify their location timeline if needed, adding manual entries when necessary. This real-time logging provides clear visibility on proximity to residency limits, facilitating better compliance and future travel planning.

Contemporaneous Digital Evidence

Court cases have demonstrated that simple day counts often do not suffice for tax authorities, who may require additional corroborative evidence. Our case study into an Irish appeal case, where the Appellant had to prove he didn’t spend enough days in Ireland to justify as a tax resident, highlights this clearly.

During the court case, the Appeal Commissioner, Mark O’Mahony, commented how a credit card transaction proves nothing but a purchase. When discussing the Appellant’s car rental receipt as proof, he said, “at best, they [the receipts] showed that the appellant had occasionally rented a car”. He continued that this transaction could well be made as a tax resident or not — it alone offers little to him to judge.

To address this, Daysium allows clients to add geo-tagged supporting documents to their location data, such as photos from significant events or notes detailing the context of their stays. This capability is invaluable, especially in appeals or where detailed historical proof is necessary, enhancing the reliability of the tax records and helping to justify residency claims effectively.

Benefits of Daysium for Clients and Advisors

Daysium can strengthen record-keeping and ensure robust day-counting compliance. While the developments around the UK’s non-dom status won’t come to fruition until next year, now is the perfect time to bolster your defences.

For individual Clients, Daysium offers an elegant compliance tool with the following benefits:

Enhanced Record-Keeping: Daysium strengthens compliance with robust, automated day-counting and secure generation of supportive documentation.

Immediate Access and Accuracy: Clients gain instant access to their day count, reducing errors compared to manual systems like spreadsheets.

Security and Evidence Generation: High security features ensure data protection, while the platform facilitates the creation of corroborative evidence.

Getting Started with Daysium

As the UK’s tax landscape for non-domiciled residents undergoes significant changes, staying ahead of these shifts is crucial for tax advisors and their clients. The Daysium platform provides the necessary tools to ensure compliance, offering precision in day-counting and robust record-keeping capabilities.

Individuals should reach out to their tax advisor and check if they’re partnered with Daysium. You can also take our Risk Score Assessment here and join the Daysium waitlist — although introduction through a Partner will be a faster way to get started!

If you’re an accountant or a tax advisor and would like to apply to join our Partner Program, fill out our scorecard, to see if we’re a perfect fit.

Embracing Daysium not only simplifies the transition under the new regulations but also positions your practice to deliver proactive, strategic advice in this evolving environment. Now is the time to integrate this innovative solution and secure a competitive edge in the realm of international tax advisory.

Navigating Tax Compliance Challenges: A Case Study of the UK’s Statutory Residence Test

In the complex world of tax compliance, the UK’s Statutory Residence Test (SRT) presents a significant challenge, particularly for globally mobile individuals. This case study explores the intricacies of the SRT and illustrates the tax compliance challenges individuals need to navigate to guarantee compliance. We’ll examine a specific case involving day counting and outline the key challenges you could overcome with Daysium’s innovative day counting solution.

Overview of the Statutory Residence Test (SRT)

Since its introduction in the 2013/14 tax year, the UK’s Statutory Residence Test (SRT) has become a cornerstone in determining an individual’s tax residence status. Key provisions of the SRT state:

“(1) A person is resident in the UK for a year if either the automatic residence test or the sufficient ties test is met.

(2) The automatic residence test requires a person to meet none of the automatic overseas tests, and at least one of the automatic UK tests (para 5).

(3) Many of the automatic overseas tests (paras 12, 13 and 14), and the automatic UK tests (paras 7 and 8) depend on the number of days the person spends in the UK.

(4) If the automatic residence test is not met, the “sufficient ties” test applies.

(5) Under the sufficient ties test, a person’s residence is determined by a combination of (a) the number of UK ties and (b) the number of days the person spends in the UK.

(6) The number of ties sufficient to make a person UK resident depends on (a) whether the person was resident in the UK for any of the previous three tax years, and (b) the number of days the person spends in the UK in the tax year in question (para 17(3)).

(7) The combinations of days spent in the UK and the number of ties are set out in Tables at paras 18 and 19.”

Day counting is essential to the tests, both for the automatic residence test and the sufficient ties test. Para 22 of SRT determines how many days a person spends in the UK.

Generally, a person is present in the UK for day-counting purposes if they are present at the end of a day.

The exceptions to the general rule are:

Transit Exception: A day does not count if the person only arrives in the UK as a passenger, leaves the next day, and engages only in transit-related activities.

Exceptional Circumstances Exception: A day does not count if the person would have left the UK but was unable to due to exceptional circumstances beyond their control, intending to leave as soon as possible. Exceptional circumstances might include emergencies like war, natural disasters, or severe health issues.

There are also limitations on the number of days a person can spend in the UK for exceptional circumstances each tax year, which are capped at 60 days.

However, the case we’ll discuss shows that what counts as ‘exceptional’ is ambiguous at best.

Introducing the Case Study

The Appellant in the case was a taxpayer who moved from the UK to Ireland on April 4, 2015. In her self-assessment tax return for the year 2015/16, she claimed non-UK residency.

HMRC challenged this decision because she had spent more than the permissible number of days in the UK, which led the taxpayer to appeal to the First-tier Tribunal (FTT).

Both the Appellant and the authorities agreed that the Appellant had spent 50 nights in the UK during the tax year. This was more than the 45-day limit set by SRT.

However, the issue became the exceptional circumstances clause, which allows some leeway in the day count. The test allows certain days to be disregarded in the SRT day count when a person (P):

“(a) P would not be present in the UK at the end of that day but for exceptional circumstances beyond P’s control that prevent P from leaving the UK, and

(b) P intends to leave the UK as soon as those circumstances permit.”

The Appellant argued that her presence in the UK was beyond the allowed 45-day limit due to such exceptional circumstances. Her twin sister suffered from severe alcoholism and depression, which led to suicidal threats that forced her to be present in the UK for those extra five days. She further argued that she had a duty of care towards her sister’s young children and had to stay in the country for these additional days.

HMRC argued that her account wasn’t warranted by exceptional circumstances, and as such, she was to pay income tax in the UK as a tax resident. The additional tax due would amount to £3,142,550.58 — a considerable sum to pay.

The Appellant’s Challenge — A Taxpayer v HMRC (2022) UKFTT 00133 (TC)

The FTT heard the case in 2022, ruling initially that the exceptional circumstances cited, specifically her sister’s alcoholism and depression, did not exempt the Appellant’s days spent in the UK. However, the FTT justified her secondary argument that she needed to care for her dependent minor children. Thus, her appeal was approved and the Appellant was deemed non-resident for tax purposes.

Initial Decision and Repeal — The Commissioners for HMRC v A Taxpayer (2023) UKUT 00182 (TCC)

HMRC appealed the FTT’s decision. This led to reconsidering whether the exceptional circumstances were valid and met by the taxpayer.

Ultimately, the higher tribunal allowed HMRC’s appeal, agreeing with their position and dismissing the taxpayer’s appeal. Consequently, she was deemed a UK tax resident for 2015/16.

Day Counting Challenges and the Exceptional Circumstances Clause

The historic case highlights several important lessons on day counting and record-keeping to ensure tax compliance.

Location accuracy

While the accuracy of the day count wasn’t at the heart of the appeals, location accuracy was considered to determine the status of the exceptional circumstances. During the appeal process, it was evident that the Appellant didn’t always provide the most accurate representation of her location. This led to HMRC initially questioning whether these days were spent for exceptional circumstances and care for the twin sister.

The issue is that the proof of evidence relies on the Appellant. However, these investigations, initially and primarily the subsequent appeal to repeal the original decision, happened years after the events under scrutiny.

Proof of activity

The second consideration is linked to location accuracy. The evidence of activity during the Appellant’s time in the UK was intensely scrutinised. The Appellant produced credit card transaction data to show where she was but often couldn’t provide any further evidence as to why she was there.

For example, the judge points out that the Appellant’s card was used at a children’s hospital in Manchester. But the Appellant couldn’t provide details about what that visit was for. As such, it was considered part of an evidence trail showing that her appearance in the UK wasn’t exceptional.

The prolonged process

The above are two core issues at the heart of the case. However, there are a few broader lessons to be learned from it.

First, the lack of robust evidence and accurate day counting can prolong tax investigations. An inaccurate day count without robust evidence can launch an investigation. The investigation can drag on if the evidence isn’t solid and ready.

Furthermore, HMRC isn’t afraid to further push its side of the story. The administration was unhappy with the first ruling and continued interpreting the rules around SRT differently, making this case go to the upper court.

The case dealt with a tax return for the year 2015/16, with the first tribunal taking place in 2022. The second appeal case occurred a year later, in 2023. The timeline shows how long these investigations can take, meaning the Appellant had to live in uncertainty for almost seven years.

Planning the day count

The Appellant admitted that her tax advisory team told her of the day count limits before the move. She was advised to keep an accurate day count and was aware of the limits she was under.

While she clearly argued that her stays resulted from unexceptional circumstances, it is worth noting the importance of keeping track of the day count. Speculation on how the Appellant counted her days in the UK is not the intention.

Don’t keep accurate real-time records of your travel days. Entering your travel dates after travelling can result in inaccuracies or delayed counting. You might be close to your limit or accidentally step over it sooner than you thought.

Don’t allow you to plan ahead. These tools don’t always make it easy to plan ahead and know how close you are to reaching your limit.

The Role of Daysium in Enhancing Compliance and Accuracy

The historic ruling laid some concerning precedents regarding exceptional circumstances. Having an upper court overrule an earlier decision shows that there remains much ambiguity in the world of tax compliance. Many HNWIs must understand the risk of an inquiry when navigating tax compliance challenges.

As the challenges of accurate day counting and proof of exceptional circumstances emerge from this case, Daysium’s capabilities could offer substantial relief. By automatically logging location data and providing real-time day count updates, Daysium helps ensure compliance and simplifies the management of residency requirements.

Daysium’s role as a tax compliance tool would:

Create evidence to prove location. Daysium automates evidence collection, logging your location data automatically into a timeline. You will have a centralised digital location record, and the system will update your day count in real time.

Attach proof of activity to your location data. Supplementary evidence, such as geo-tagged photographs and receipts, can strengthen your location logging and fortify the authenticity and reliability of your claim. In exceptional circumstances, you can generate a more substantial case by including additional notes to create a more compelling narrative of your day count.

Reduce enquiry times. The robust evidence you’ve generated can make the enquiry process smoother and faster. The data will help the tax advisory team to build a stronger case and deal with any enquiries by the authorities faster.

Stay aware of your day count. Real-time calculation of day count enables you to proactively manage your situation. The information isn’t inaccessible and hard to find—everything is available in the palm of your hand. Therefore, you can better plan and manage your day counting even in exceptional circumstances.

Count based on your individual situation. Daysium’s day counting is always personalised around your specific needs. We’ve encoded the SRT ruleset to our platform, amongst many other global tax rulesets, meaning your day counting is specific to you, and you can configure it if your situation changes.

Navigating Tax Compliance Challenges in a Global Context

Tax authorities worldwide are focusing on the tax affairs of globally mobile individuals. They are increasingly using sophisticated methods, including AI tools. Interpretation of the existing rules is putting many individuals under the microscope. At the same time, the length of enquiries is increasing, leading to longer and more complex processes. The prolonged investigations can be taxing, not just financially but also emotionally.

With Daysium’s platform, you can:

Enhance your compliance. The robust record-keeping capabilities enable you to navigate recency requirements precisely and confidently.

Reduce your risk of investigation. Improved compliance reduces the risk of time-consuming investigation. Real-time access to day counting and reports will help individuals identify potential issues immediately, guaranteeing that tax advisory teams can help improve compliance.

Strengthen your defence. The comprehensive data repository you’re creating will expedite the resolution process. You’ll save time and resources not only for yourself but also for the tax authorities. You can more confidently show what your day count is and what evidence you have to prove it, especially in exceptional circumstances.

In conclusion, as tax authorities globally enhance their scrutiny using sophisticated technologies, solving tax compliance challenges becomes increasingly complex. Daysium stands at the forefront of this landscape, offering a robust, innovative solution that ensures compliance and transforms it into a strategic advantage for globally mobile individuals. Your records are robust, and if you face an investigation, you can expedite the process by confidently saying, “There’s nothing to see here, everything is in order”.

Case Study: Navigating Tax Residency Challenges with Daysium

Accurate record-keeping can reduce your risk of a lengthy and costly tax investigation. Cases where investigation and even an appeal have been carried out and ruled in favour of the individual are prime examples of how robust evidence can alleviate tax residency challenges.

We wanted to examine the impact Daysium’s innovative way of gathering evidence could have on reducing the risk of an investigation. Luckily, one of our Founding Partners, Stephanie Wickham, an award-winning international and expatriate tax specialist who founded Expat Taxes in Ireland, directed us towards two intriguing court appeal cases from Ireland.

A closer look at the cases showed how our platform could lower risk—not only in terms of strengthening compliance but also resulting in a strong trail of evidence to hasten the actual enquiry process.

Introducing the Two Cases

The cases in question were adjudicated in Irish courts in 2019 and 2020.

Case A – 177TACD2020

In this case, a numismatist was required to demonstrate his non-tax residency in Ireland between 2002 and 2006. He bore the responsibility of proving to the courts that he did not:

Stay in Ireland for 183 days or more during any single year.

Spend a total of 280 days or more in Ireland over two consecutive years.

Central to the case was the need to substantiate his physical presence outside Ireland and the nature of his income.

The appellant contended that he did not spend sufficient time in Ireland during those years to be considered a tax resident. Despite being domiciled in Ireland, he argued that his time spent outside the country exempted him from tax liability.

Case B – 08TACD2020

On the other hand, Case B presents the story of a UK citizen who resided in Northern Ireland but commuted to work in Ireland.

These work commutes occurred from August 20, 2012, to May 10, 2013. Subsequently, from May 11, 2013, to November 5, the appellant lived in Ireland before returning to the United Kingdom.

He asserted his tax residency in Ireland for 2012 through an elective declaration. Additionally, he argued for tax residency in 2013, citing his presence in Ireland for over 183 days that year. He also claimed split residence for 2012 and 2013.

Identifying the Tax Residency Challenges

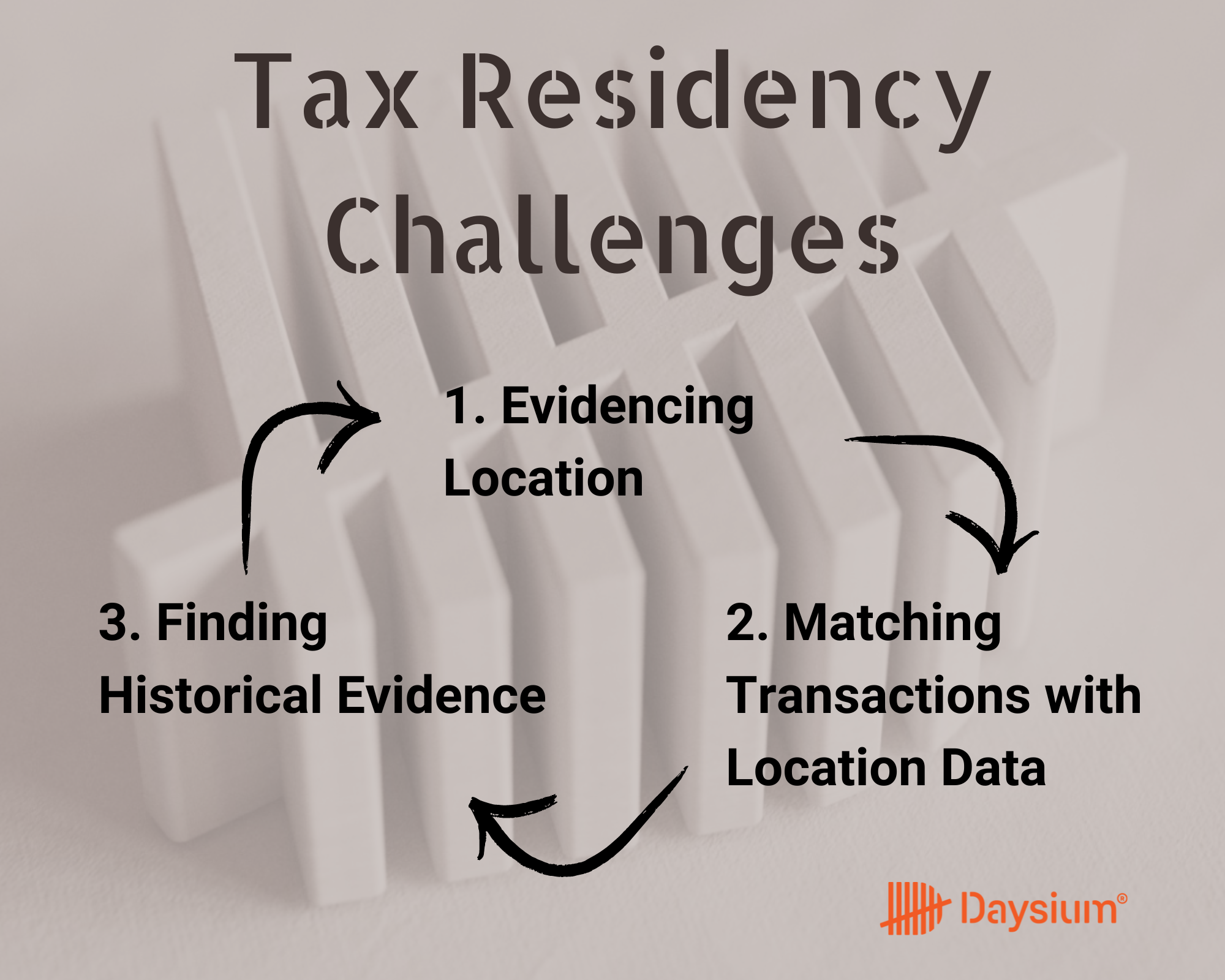

The cases of Case A and Case B unveiled three fundamental challenges individuals encounter in asserting tax residency:

Evidencing Location

The main issue for Case A was for the appellant to show his whereabouts. For the authorities, it’s not enough to claim that “I was here”; you have to find evidence to prove that.

In Case A, the appellant’s connection to various countries complicated matters. He had several addresses attached to his name, proving residence wasn’t straightforward. During the proceedings, the appellant relied on showcasing his location through receipts from car rentals, restaurant bills, and credit card transactions.

Matching Transactions with Location

Additionally, as the cases show, a transaction alone may not be enough evidence of your location. In Case A, the appellant’s documents resulted in a fragmented and inconsistent trail of proof. The Appeal Commissioner, Mark O’Mahony, determined at the start of the opening analysis how the documents didn’t prove anything but a purchase.

For example, regarding a car rental receipt from an Irish airport, O’Mahony notes that “at best, they showed that the appellant had occasionally rented a car”, which, he continued, “could as easily be done by a tax resident as by a non-resident.”

Similarly, a credit card statement of a purchase placing you in another country is not substantial proof. Credit card transactions might not always go through at the time of purchase and could be used to make online purchases.

Finding Historical Evidence

Finally, both cases showcase an issue of searching for historical evidence. The cases involved prior years, with the court appeals taking place years later. In Case A, the proof required dates back almost a decade.

Searching for evidence dating that far back proved a challenge. The appellant for Case A admitted that his day counting records might not be accurate, and during the appeal process, witnesses sometimes offered contradictory evidence.

Although both cases were ultimately ruled in favour of the appellant, the process to reach a favourable outcome has the potential to be faster. The risk of the enquiry and the costs associated with it could have been avoided with Daysium.

With its innovative features and robust capabilities, Daysium revolutionises this kind of tax compliance in three key ways:

Strengthening Record-Keeping: Daysium automates evidence collection, generating a comprehensive digital trail of activities and locations. Your location data is logged automatically, clearly showing your day count. Record-keeping is centralised, with digital records accessible and secured with the best encryption techniques.

Displaying Location with Other Evidence: By integrating location data with supplementary evidence like geo-tagged photographs and receipts, Daysium fortifies the authenticity and reliability of your claims. The platform’s seamless integration of disparate data sources creates a compelling narrative that it was indeed you who was, where you now say you were.

Informing of Current Situation: Real-time calculation of day counts enables you to proactively manage your day count status, ensuring compliance with relevant tax rules and regulations. By providing accurate, up-to-date insights into your status, Daysium empowers you to make informed decisions and mitigate compliance risks effectively.

As an expatriate tax specialist, one of our founding partners Stephanie Wickham agrees with how Daysium can help in today’s tax landscape. She notes,

“Tax authorities are increasingly using more sophisticated data analysis in their audit interventions and risk management. So for clients that frequently cross borders a platform such as Daysium is invaluable in ensuring that a solid evidence book can be presented in the event of a Revenue enquiry/intervention.”

-Stephanie Wickham-

Unleashing the Potential Benefits of Daysium

In both these cases, the adoption of Daysium would have offered three critical advantages to the appellants to navigate their tax residency challenges.

Enhanced Compliance: Daysium’s robust record-keeping capabilities enable you to navigate residency requirements precisely and confidently, ensuring adherence to relevant tax regulations.

Reduced risk of enquiries: As compliance becomes more accessible to navigate, the risk of a time-consuming enquiry lessens. Maintaining day count becomes more accessible, and you can better identify any potential issues with your residency data together with your tax advisory team.

Efficient Investigations: If you come face-to-face with an inquiry, Daysium’s comprehensive data repository expedites the resolution process, saving time and resources for you and the tax authorities. The platform’s seamless integration of disparate data sources facilitates faster, more efficient investigations, enhancing regulatory compliance and enforcement efforts.

In conclusion, Daysium stands at the forefront of tax compliance innovation, offering a transformative solution to the challenges of keeping a robust set of records. With Daysium, navigating complex tax regulations becomes not just a requirement but a strategic advantage in safeguarding your financial interests and ensuring regulatory compliance.

You can trust your records to be robust, and if the authorities reach out, you and your team can confidently say, “There’s nothing to see here, everything is in order”.

Navigating Tax Residency: Solving the Challenge of Counting Days

We don’t think the old way of counting days is working. Tax advisors are pushing clients to improve record-keeping for tax residency compliance, while clients are trying to keep up with the different rules. There is too much margin for error, inaccuracies and frustration out there.

Let’s solve day counting by looking closely at some of the main pain points to navigate. By the end of this article, we’ll show you how to solve the problem with day counting with Daysium.

Let’s look at the following topics:

What is Tax Residency?

The Organisation for Economic Cooperation and Development’s (OECD) definition says tax residency “is determined under the domestic tax laws of each jurisdiction”.

Its two main functionalities are:

To decide whether you are liable to pay tax in the jurisdiction where you spend time.

To determine the scope of your liability.

Tax residence is crucial because it will decide where and when to pay tax. In a global world, and as a global citizen, determining residency can be trickier. If you spend significant time abroad, you may expose yourself to different jurisdictions. You must know the rules in different jurisdictions to ensure proper tax planning.

Your residence matters because:

The right to reside in a country, permanently or temporarily, doesn’t automatically make you a ‘tax resident’.

You might not be liable to pay taxes to the country where you have citizenship.

You might have to pay tax in two jurisdictions: where you work and reside.

Is Domicile the Same Thing as Residence?

No, but your domicile can impact your taxation. Domicile is a historical legal concept still used. You’re domiciled in the country to which you are most closely connected. For many, it is where you were born or have a permanent home. You could think of it as the place you intend to return to, even if you’ll spend time somewhere else in between.

Your domicile can impact your tax status and determine where and how much you pay. It’s important to note that your domicile status might make it so that you don’t pay tax on certain assets to your tax residency country.

You can acquire a domicile of choice. However, the process can vary between jurisdictions. We always advise contacting tax experts if you’re interested in learning more.

What are The Different Conditions to Determine Residency?

Jurisdictions use different criteria to determine residency, ranging from your time in the country to your ties to it. The rules introduce the first layer of complexity to your day counting.

The amount of time you spend in different jurisdictions can change yearly. Since tax residency is evaluated annually, you must know how many days you spend in different countries.

Let’s look at the two critical conditions:

Days Spent in the Country

The critical factor for most jurisdictions is how many days you spend in the country. You are a tax resident if you pass certain days – no matter your reasons. Many countries use the 183-day threshold. For example, in the UK, one condition of the residency test is that you spend 183 days in the country during a tax year.

But countries add a layer of complexity to day counting. You may need to meet several other conditions in the UK and elsewhere, aside from time spent.

Substantial Presence or Ties

Jurisdictions also look at your presence and ties within a country to determine tax residency. The criteria don’t count only the days you spend in the country but other factors. These can include things:

Where is your permanent home?

Where do you work?

How many family ties do you have to the country?

What other vital interests do you have in the country?

For example, the UK has a condition where you’re likely treated as a UK citizen if you own a home in the UK and no home overseas.

Double Taxation Rules

You might be considered a ‘treaty resident’ if you’re a resident in one or two double-taxation signatory countries. Tax treaties are in place to prevent double taxation. Your tax advisor can help you understand how double taxation rules may apply to you.

What is the Main Challenge With Day Counting?

The main challenge in day counting is the different methods jurisdictions use to determine a ‘present’ day. Countries vary widely in their methodology, meaning that you need to be aware of the intricacies of the rule to get your day count right.

Let’s take the example of Ireland and the UK. In Ireland, you are considered to have been ‘present’ for a day if you were in the country at any point.

Suppose you are in Ireland on the 12th. The day would count as a day for residency calculations, even if you flew in or out of the country at any time during the day.

But UK’s legislation considers ‘present’ differently. A day only counts towards your tax residency days if you were in the UK at midnight. If you fly out on the 12th before midnight, the day won’t count.

Therefore, you can’t solely count days when considering your tax residency. You must know the specifics of what determines your status for each day.

You should also be aware of exceptional circumstances. For example, you’re not ‘present’ if you spend time in Ireland in transit – meaning you don’t leave the airport or port. Most jurisdictions consider exceptional circumstances when counting days. A day might not count as ‘present’ due to unforeseen circumstances such as an illness or natural disaster preventing you from leaving.

Solving Day Counting With Daysium

All this complexity shows that counting days can be difficult. We also believe the traditional solutions of day counting aren’t sufficient. Holding on to boarding passes, hotel receipts, and counting days in Excel can introduce risk to your accuracy.

There is a better way to navigate tax residency and day counting.

Daysium can help you with the following:

Set up Automated Systems Based on Your Personal Needs

Most tools might help you count days, but do they understand your situation? With Daysium, you and your tax advisor can set up parameters that matter to you. Your tax advisor can set the rules to make counting days accurate and designed around your needs.

Monitor Your Day Count Fast and Efficiently

Our platform’s app allows you to see your current day count in the palm of your hand. If you’re considering travel but are worried about overstaying, you can check your situation within seconds. You’ll have the confidence and freedom to make those travel decisions for business or leisure.

Prepare Your Records for Tax Inquiries

Jurisdictions employ different tests to check your residency status. Authorities also monitor whether day counting is accurate, especially for high-wealth, mobile individuals. Traditional record-keeping has its problems that we at Daysium want to change.

We log your data securely, creating a trail of proof to prepare your records for tax inquiries. The corroborating evidence is for your eyes only unless you want to share it with your tax advisor. The data can help when you need to prove you’ve counted the days correctly and spent time where you said you did.

Join the Waitlist Today

Complexities can be solved, and we’re committed to helping you do that. We understand the intricacies of navigating the different jurisdictions. But we also know that clients and advisors are the experts in their situations. We want to empower you to make informed decisions and stay prepared for whatever the future brings – dealing with a tax inquiry or a change in residence.

We’d love to have you join this revolution in day counting. You can’t buy our app on the App Store, but you can join the waitlist.

If you’re a tax advisor and interested in how we can transform your clients’ compliance journey, we’ve recently opened our Partner Program. Click here to see if we’re a perfect match, and let’s transform tax compliance together!

Revolutionising Record-Keeping: How Technology is Transforming Tax Compliance for Individuals

Picture the scene: your tax advisor calls and informs you of a coming tax inquiry. You’re required to gather your records – flight itinerary, hotel receipts, photos. Documents showing your residency days at a given jurisdiction.

The scenario is not uncommon. An HMRC spokesperson said their investigative team secured £4bn from the wealthy, an increase of 60% from the previous year. You’ll need accurate records to prepare yourself for the investigation.

The good news is that technology is revolutionising record-keeping. Let’s take a look at how by discussing the following topics:

Three Reasons for Accurate Record-Keeping for Tax Purposes

Let’s start by considering why you should have record-keeping on your radar for tax compliance purposes.

Accurate record-keeping is more than about saving time. It can be vital for financial planning and keeping the taxman happy.

A pristine set of records will help you with:

1. Compliance with Tax Laws

The dynamic nature of global residency calls for discerning your movements across jurisdictions. Consider the complexities: the definition of tax residency varies from country to country. For example, counting residency days in Ireland differs from that in the UK. Knowing one jurisdiction inside out can lead to misinterpretation in another.

For example, the UK and Ireland count a residency day slightly differently. In Ireland, you are considered ‘present’ if you’re in the county at any time during the day. However, in the UK, you’re considered ‘present’ if you were in the UK at midnight at the end of the day.

Depending on what jurisdictions matter to you, the intricacies of understanding the rules are vital for compliance.

Documenting your days in different jurisdictions is one thing. But as local governments are increasingly interested in the tax affairs of the wealthy, you often need to go further. Tax compliance requires documenting your travel itineraries, including precise arrival and departure times. The proof can safeguard you against inadvertent errors that could lead to legal complications.

2. Tax Inquiry Preparedness

The scrutiny and regulatory oversight are increasingly focused on high net worth individuals ( HNWIs). The UK even has a Wealthy Team examining the country’s wealthiest taxpayers. In 2022, they opened 25 criminal investigations.

Meticulous records prepare you for an inquiry that could happen. Suppose you have corroborating evidence to show things like your location data. In that case, you have irrefutable proof of adhering to tax laws. Access to the information can give you peace of mind before and during an inquiry, moving things along swiftly.

3. Freedom to Choose

Accurate data enhances your freedom, whether you travel to another business meeting or spend time with family abroad.

Imagine a scenario where you receive an invitation to an exciting new business opportunity. But you’ve already spent time in the UK and you’re worried you might overstay. If you’re guessing your current day count, you may end up with one of two bad scenarios. You might travel to the meeting, overstay and pay more tax. Alternatively, you don’t risk it; stay home and miss out on the opportunity.

Meticulous records give you more freedom to make informed decisions and spend time how you want.

The Problem with Traditional Record-Keeping

Record-keeping makes sense, but not all methods are the same. We’re talking about traditional record-keeping – your Excel spreadsheets and cabinet full of binders, if you will.

The core problems for traditional, manual methods are:

Human error – To err is to be human, but unfortunately, sometimes these errors cost. The risks increase the more delegation record-keeping involves. When you have tax advisors dealing with PAs, communication errors could occur.

Access – Manual folders don’t travel with you, no matter how well you organise them. You also need to consider who can have access to these files. Physical access has many hurdles to overcome. The cost of keeping your files safe is often at the top.

Data loss – Physical copies can and will get lost. This could be due to accidents or even nefarious acts. The fact you can’t immediately have all records centralised is a risk.

Compliance risks – Tax laws and regulations change constantly. Monitoring compliance becomes difficult when records are manually kept.

Your reliance on traditional record-keeping doesn’t cut it for one more reason: the authorities aren’t relying on it. Jurisdictions worldwide are using digital tools to combat things like tax evasion. Different agencies are communicating with each other, making it vital to have good evidence on your part.

For example, the tax authority might look into your residency records. They’ll communicate with other local authorities and notice there’s a parking ticket to a vehicle registered to your name on a day you weren’t supposed to be in the country. You need to prove you weren’t there; for this, you require solid evidence.

The good news is that technology can help you with the conundrum.

Three Technologies to Improve Record-Keeping for Tax Compliance

As tax jurisdictions are improving their use of technology to investigate and close loopholes, you should also add the right technology to your toolkit. These innovations can make controlling your time and data easier, leading to more peace of mind.

1. Mobile Apps

A wealth of mobile apps is on the market to help gather and log data. In general, many platforms can connect different accounts under one central view. These traditional finance apps can make monitoring your accounts easier. Tax jurisdictions, like HMRC, also have apps to let you study your tax data.

The market also has a few record-keeping apps for counting your days in different tax jurisdictions. While these can help you get an overview of days spent abroad, they don’t go far enough. Our app facilitates logging your residency days, creating a trail of records to help in the case of an audit.

You can log in any data that you find valuable to show and prove your location. You’ll not only get a record of your days in a specific country and jurisdiction, but also evidence to support the claim.

2. Cloud-Based Platforms

Cloud solutions are another big technology revolutionising tax compliance and record-keeping. The cloud enables you to:

Centralise your tax data.

Access your records no matter your location.

Collaborate faster with your tax advisor.

Choose who can access the data and what data they can see.

Improve data security, with information stored in secure servers.

Take our Daysium app as an example. The app travels with you wherever you go. You can also share reports with your accountant, whether in the same country or not. But these reports are never automated. We believe you should be in charge of what and when you share.

3. Automated Record-Keeping

When your tax advisor asks for specific records, knowing where to start can seem daunting. Finding corroborating evidence after an event took place months ago is time away from family or work.

Combining the cloud with artificial intelligence and machine learning transforms the process. You can automate many record-keeping processes for tax purposes. When you add AI to the mix, you can also process vast amounts of data, receiving in-depth analysis of what’s happening.

We have our AI assistant, Daysi, who we describe as an extension of your tax advisor. The always-present assistant you can turn to if your tax advisor isn’t available. Daysi can answer your questions and help give you an idea how to solve a problem – and tell you to reach out for your advisor when needed. You’ll get extra support to navigate your record-keeping issues.

The Benefits of Using Technology for Tax Compliance

All of the above three technological solutions come with benefits. Adopting them to your tax record-keeping can help you:

Save time – AI can help automate many processes you previously had to do manually. You don’t have to browse through filing cabinets to find a slip; you can simply search your digital records in minutes.

Reduce errors – Humans make mistakes. While you could write down the wrong date from your booking reference, an app would scan it accurately.

Improve access – The increased access to the cloud means you can take care of tax matters anywhere in the world. Your tax advisors can also access your information without compromising the security of the files.

The above technologies and their benefits ultimately lead to cost savings. You empower yourself to make the most of your tax code and leave room for other things in life – business or family.

Best Practices to Overcome the Risks of Digitalising Your Record-Keeping

In a UK Government survey, 45% of UK adults disagreed with the statement that they feel safe and secure online. Cyber-attacks and scams are still a big issue when using technology and digital platforms.

Dread of digital safety isn’t unreasonable. AON’s survey from 2023 shows one in five businesses in Ireland experienced a cyber attack in 2022.

However, awareness of the possible risks shouldn’t be a reason to stop using technology. The perception can aid you in being smarter with your digital choices.

HOW CAN YOU GUARANTEE YOU’RE SAFE?

The three best practices to digitise record-keeping the right way are:

Choose the right products and platforms. When looking for a product or app, pay attention to security issues. Check what the company says about the security features and ask questions if you can’t find the answers upfront.

Manage access. Use the option to manage and control access to your data. Ensure you understand who can access your data and how the platform stores it. The more control you have over who has access, the better.

Understand relevant regulations. Local authorities set clear rules on how to keep records. Be aware of these rules and ensure all your technologies comply. Again, talking to the service provider is essential to know whether it complies with the regulations.

If you’d like to understand your current risk level better and get actionable steps to improve, take our Risk Score Assessment here. The quick assessment will reveal any problem areas in your current record-keeping and suggest ways to strengthen those areas.

A Case Study: Using Daysium to Revolutionise Your Tax Record-Keeping

We at Daysium are confident technology can revolutionise tax compliance. Our platform offers HNWIs a way to monitor how many days they spend in or out of jurisdictions relevant to their tax residency. With our app, you can:

Establish rules to follow regulations relevant to you and you only.

Plan your future travel to ensure you don’t break the rules.

Log travel in a timeline to avoid data gaps in your tax records.

Provide evidence to support your tax residence claim, making audits faster and smoother for all involved.

Generate reports that can be securely shared with your advisors.

We use automation and cloud solutions to smoothen the above steps for you. You don’t need to spend hours adding information to our app. The automated process enables you to view your day count accurately and in the palm of your hand.

Did you get a call to attend a meeting on the other side of the world? With Daysium, you don’t have to fear missing out on this opportunity. You can look at your profile and see if you can accept it or schedule it for another time.

And you don’t need to worry about security. Daysium doesn’t sell your data or share it with anyone. You can control who gets access to the reports you generate. You are at the helm of this technological revolution, not a bystander. We like to think we are the guardians of your data.

Conclusion

Meticulous record-keeping for tax purposes ensures compliance with increasingly complex tax laws across jurisdictions. Technology can help you prepare for tax inquiries, providing irrefutable evidence to support your adherence to tax laws. The process will be smoother, and your mind will be at ease.

As authorities rely more on digital toolkits, adopting technology also becomes vital for you. Knowing things like your location data optimises your time.

At Daysium, we aim to empower you to control your data better and help you navigate record-keeping efficiently. If you want to know more about our platform, contact us and join our waiting list today.