Non-dom Plans: Are the Wealthy Leaving the UK?

The UK’s wealthy, non-domiciled (non-dom) individuals find themselves at a crossroads. Faced with upcoming changes to the regime, many are weighing up their options. Should they stay and adapt to new tax obligations or seek a more favourable tax regime abroad?

The UK’s shift signals a new era for non-doms. An era where strategic planning is crucial. We asked our Founding Partners for their opinions on non-dom plans. Here’s a closer look at what UK non-doms are considering—and why now may be the time to reassess tax residency.

What are non-doms planning?

The reactions to proposed tax changes have varied, painting a complex picture of what lies ahead. Historical patterns show a tendency for non-doms to stay put.

According to research funded by the Economic and Social Research Council, scrapping the non-dom regime would likely have only a modest impact. Their research estimates that only around 0.3% of non-doms would leave. The study drew on data from similar reforms in 2017 when just 0.2% of long-term non-doms and approximately 2% of recent arrivals opted to exit the UK.

Despite these figures, most tax advisors highlight that many HNWIs feel uncertain and frustrated by the new direction. Our Founding Partners’ discussions with clients reveal a similarly mixed mood. Many of their Clients question the UK’s commitment to a favourable environment for global wealth. Some are actively looking to leave, while others are still considering their options.

“I think the ones who will leave will have a sizable impact. I also think it will impact on the length of time those arriving in the country will choose to stay moving forwards.”

-Laura Sant- Director, LSR Partners , UK

The availability of a tax-efficient framework, such as the non-dom regime, is a critical consideration for many. Therefore, the ultimate decision depends on the final decisions from the UK government. In fact, a report by the consultancy firm Oxford Economics found that inheritance tax (IHT) on worldwide assets is a decisive factor for 83% of non-doms contemplating emigration.

The current UK non-dom regime

So, what does the current regime look like?

Today, the non-dom scheme allows individuals to opt for the “remittance basis,” paying UK tax only on foreign income brought into the UK. Income and gains that remain outside the UK are not subject to UK succession.

| Key Information about the Remittance Basis | |

| Available for the first 7 years of UK residency | |

| After, non-doms must pay an annual charge to continue using it: | £30,000 per year for those resident for 7 out of the last 9 tax years. |

| £60,000 per year for those resident for 12 out of the last 14 tax years | |

| After 15 years, non-doms are deemed domiciled and taxed like UK citizens on their worldwide income and gains. | |

The current regime also includes certain Inheritance Tax (IHT) provisions. These leave non-UK assets outside of UK inheritance tax if held in properly structured offshore trusts. Additionally, non-doms can bring foreign income or gains into the UK tax-free for qualifying investments in UK businesses—a key incentive for those investing locally.

Proposed changes to non-dom framework

But this historic framework is changing, and so are non-dom plans. The previous Conservative Government announced a revamp of the framework in spring 2024, and the new framework will be implemented on 6 April 2025. As our previous post on the new non-dom era outlined, the proposed changes are significant:

| Proposed non-dom changes | |||

| Who? | New arrivals who haven’t been UK residents for 10 consecutive years. | Existing tax residents who’ve been tax residents for fewer than four years are eligible for the non-dom regime. | Existing tax residents who’ve been residents for more than four years. |

| Taxation under the new system: | Full tax relief for the 4-year period of subsequent UK tax residence on their foreign income or gains (FIG) arising during this period. | Full non-dom relief until the end of their 4th year of tax residence in the UK. | Any newly arising FIG is fully taxed in the UK, regardless of domicile. |

| Temporary relief: | A temporary 50% reduction in FIG subject to tax in 2025/26 for those who will lose access to the remittance basis on 6 April 2025 and aren’t eligible for the new exemption regime. | Protections in cases where FIG arose in protected non-resident trusts before 6 April 2025. FIG from these will not be taxed unless distributions or benefits are paid to UK residents who’ve been here for more than four years. | |

However, these may not be the final rules. In the summer, the Conservatives lost power to the Labour Party, which proposed additional measures. The new government has outlined plans to:

- Move to a residence-based IHT system, where individuals would become liable for UK IHT on their worldwide assets after 10 years of UK residence.

- Introduce a 10-year “tax tail” under which individuals would remain liable for UK IHT for 10 years after leaving Britain.

- Remove the ability to shield assets held in trusts from UK IHT, regardless of when the trust was established.

Where are non-doms considering relocating?

With these changes looming, many non-doms are exploring alternative jurisdictions for relocation. Feedback from our Founding Partners highlights two popular regions: the Middle East and Europe. Both offer appealing tax regimes and lifestyle benefits aligning with the needs of HNWIs.

The Middle East

The UAE continues to grow as an option to traditional choices. The country attracts wealthy individuals with its zero-income tax policy. Research by Henley & Partners projects a net gain of 6,700 millionaires in the UAE in 2024, underscoring its status as a premier destination for those seeking a strategic tax residency.

Europe

Tax regimes are an important strategic tool for HNWIs. However, they aren’t the only contributing factor when thinking about relocating. Business opportunities and quality of life are important as well. For many non-doms, this means a desire to remain close to the UK to maintain connections and a similar lifestyle.

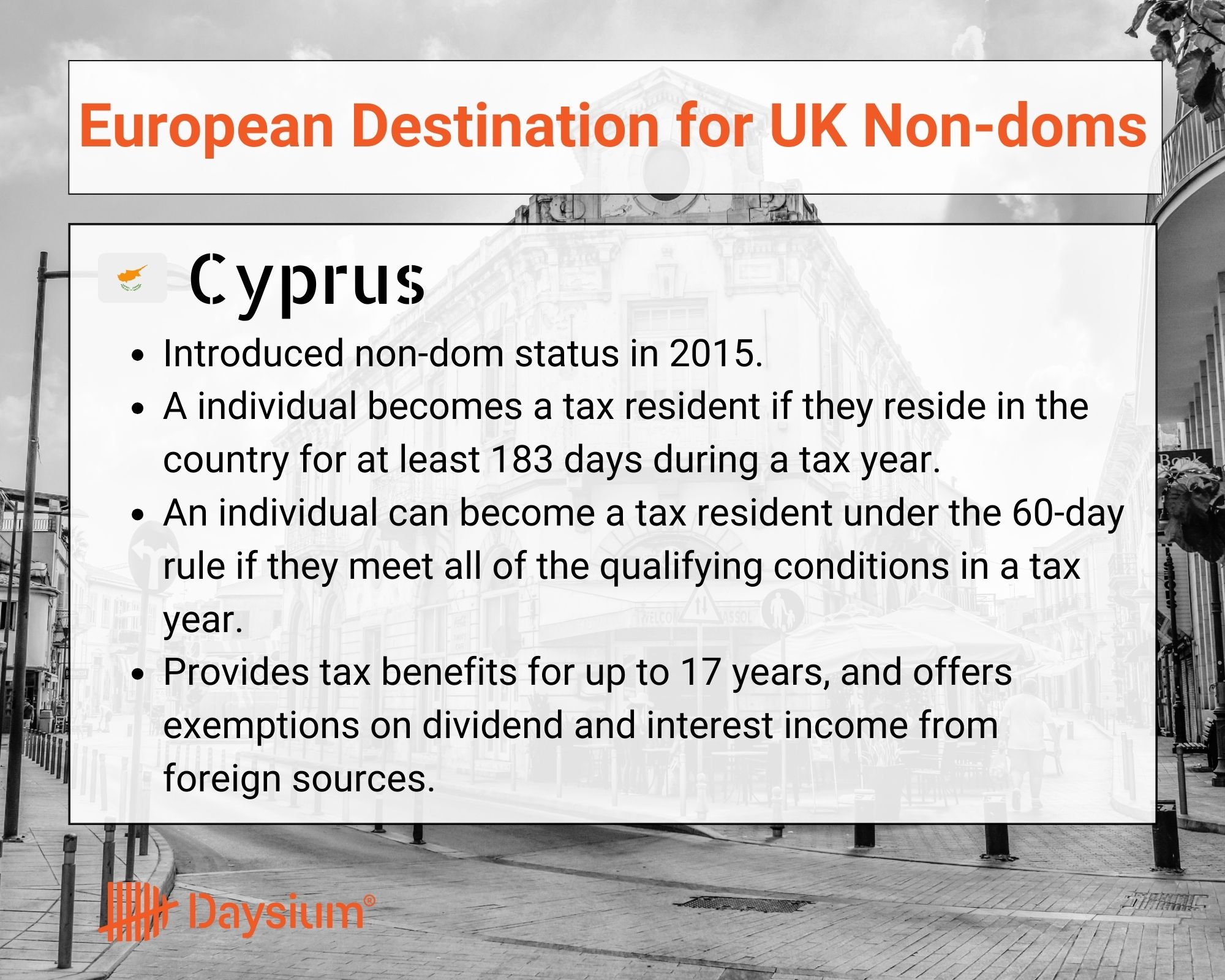

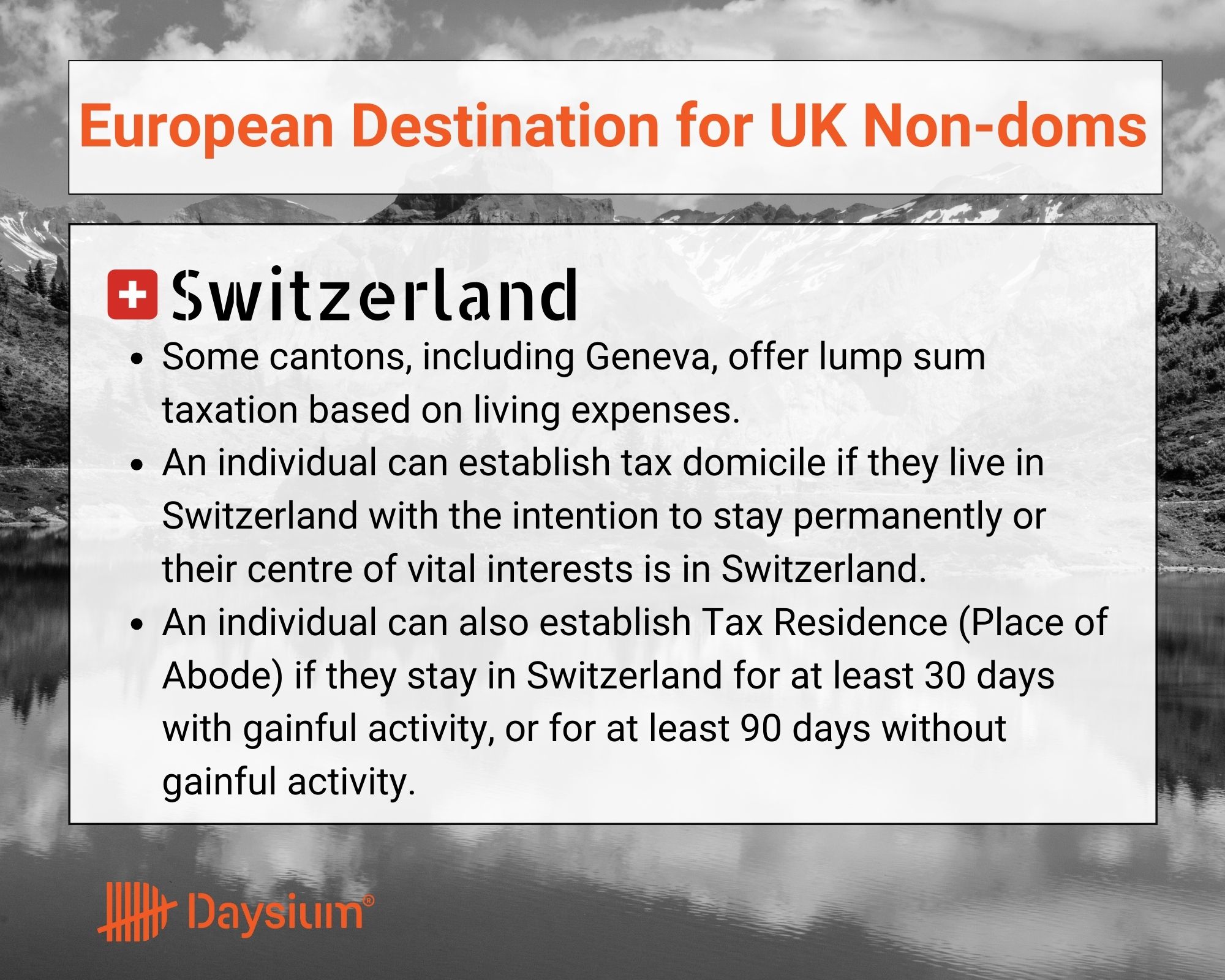

Our Founding Partners highlighted Cyprus, Switzerland, Italy, and Greece as favoured potential destinations in non-dom plans. These all offer similar lifestyle opportunities and favourable tax systems.

Fortifying tax residency compliance

The full scope of the changes remains unclear. Rumours from Whitehall suggest that the Labour government might not go ahead with all of its proposed changes. A U-turn on some of these policies could impact non-dom plans.

To prepare for the days ahead, UK non-doms or those considering a move to the UK should take steps to fortify their tax residency compliance.

Review domicile status

Conduct a formal review of your domicile position and collect evidence supporting your claims. This is crucial as HMRC is expected to scrutinise domicile status claims more aggressively.

We recommend taking our Risk Assessment for tax residency. Created together with the Contentious Tax Group, the assessment will give an overview of your current situation. Discover how likely you are to face an investigation, how ready you are to defend yourself, and what steps you can take to reduce the risk.

Evaluate investments and assets

With proposed tax changes set for April 2025, this is an ideal time to consider restructuring assets. Strategies such as realising gains ahead of time, bringing forward income, and exploring alternative investment options can help optimise your tax position under the new regime.

Consult tax experts

Working with tax advisors can ensure you maximise opportunities within the temporary relief measures and mitigate potential IHT exposure. Reviewing offshore trust structures and updating estate plans will prepare non-doms for the increased reporting requirements and help navigate this evolving regulatory landscape.

Prepare for increased reporting

Anticipate more comprehensive reporting requirements. Getting a comprehensive view of your residence status alone isn’t enough. You also want to ensure you have the data to back up your claims.

“It is possible that non-doms may want to leave the UK and take up tax residence elsewhere, but they may still want to maintain ties to the UK and visit frequently.

If so, Daysium can help you prove this by tracking your time in the UK to demonstrate that you satisfy the legislation to be deemed a non-UK resident.”

-Laurence Hodgens- Director, Hodgens Global, Dubai

Daysium can help UK non-doms plan for the future. Whether deciding to stay in the UK or immigrating elsewhere, the need to limit tax investigation threats to tax residency compliance remains vital.

Our platform and the companion app make it easy to:

- Automatically log day counts related to tax residency.

- Add supporting documentation to each entry, including flight information, selfies and transaction receipts.

- Monitor real-time day counts to better plan future travels.

The day counts aren’t just numbers going up. The platform tailors rules around individual needs, ensuring full compliance – vital when dealing with multiple tax jurisdictions.

Looking ahead

With global tax scrutiny on the rise, non-doms must proactively manage their tax residency strategies. The upcoming changes to the UK’s tax landscape signal a pivotal moment for HNWIs. Daysium’s innovative platform supports non-dom plans through this transition. We’ll provide you with convenience to navigate complex tax residency day counting rules.

Take control of your tax residency today — begin with our Risk Score Assessment and secure your future compliance.