HMRC tax investigations into individuals can be complex, time-consuming and emotionally draining, particularly for high-net-worth and globally mobile individuals. This article explores whether investigations are getting longer, why the wealthy face greater scrutiny, and how strong compliance records and automation can significantly reduce their impact.

For high-net-worth individuals (HNWIs), few things are as unsettling as a letter from His Majesty’s Revenue & Customs (HMRC), and few things are as disruptive for their advisors to manage.. Even when you are confident that your affairs are in order, the prospect of a tax investigation raises immediate concerns:

How long will this take?

How intrusive will it be?

How much time, money, and emotional energy will it consume?

Discussions about HMRC tax investigations have increased in recent years. Anecdotally, these investigations seem to be dragging on and becoming more complex. But is this really the case? And are our global lives to blame?

We’ll be looking at tax investigations on private individuals in this article, separating facts from fear. While tax investigations may sound like something that would never happen to a client, we’ll challenge this assumption and show how proper records, frameworks, and technology can protect both clients and advisors from a drawn-out, disruptive investigation.

Key Takeaways

HMRC investigations into individuals are becoming more complex — particularly where global mobility, residency, or cross-border income is involved.

Lengthy investigations are rarely about wrongdoing; they are more often driven by gaps, inconsistencies, or the need to reconstruct historical records.

Wealthy individuals face greater scrutiny because their tax affairs are higher value, more international, and more open to interpretation.

Strong, contemporaneous records can significantly shorten investigations, reducing cost, disruption, and stress.

Automation and technology are increasingly essential, not to avoid scrutiny, but to respond efficiently and confidently when it arises.

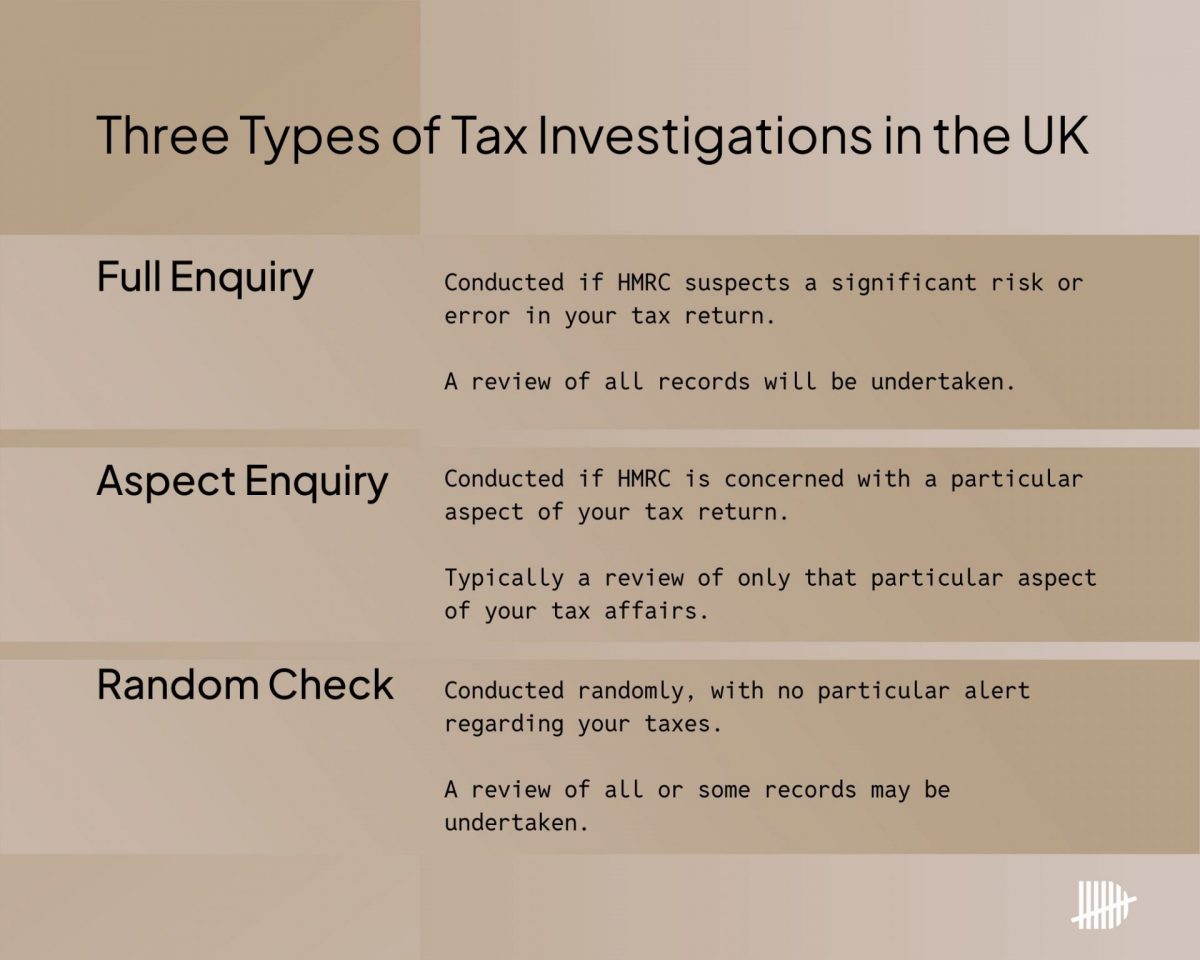

Tax enquiries vs tax investigations: Why cases escalate

Tax advisors are well aware that HMRC and clients often use the terms’ enquiry’, ‘compliance check’, and ‘investigation’ interchangeably in practice. What matters less is the label, and more when and why a case expands in scope.

In many individual cases, HMRC begins by seeking clarification on a narrow point, based on their internal data checks. These can include changes in residency positions, travel days that don’t match their records, or AI-based social media profiling where the lifestyle you show doesn’t match the client’s tax filing. Where information is clear, consistent and readily available, these matters often remain contained.

Escalation typically occurs when HMRC encounters delays, inconsistencies, or an inability to evidence facts with confidence. Gaps in day-count records, conflicting narratives across advisors, or reliance on reconstructed estimates can all signal increased risk, prompting HMRC to widen the enquiry across multiple years or issues.

From an advisor’s perspective, the practical distinction is this: enquiries become investigations not because of intent, but because of friction. The more effort required to establish basic facts, the more time and resources HMRC is likely to commit, and the longer the case tends to run.

How long can HMRC tax investigations last?

There is no fixed statutory limit on how long an HMRC tax investigation can last once it has been opened. However, there are limits to when HMRC must normally open an enquiry. For cases involving individual tax affairs, enquiry must typically be filed within 12 months of a tax return being filed (or within 12 months of the statutory filing deadline).

Even where no enquiry was opened in that time, HMRC may still raise an assessment later. These can be raised as long as up to 20 years if the loss of tax is considered deliberate; shorter limits are used for careless or unintentional cases.

During the tax enquiry, HMRC does specify a response period (usually 30 days initially). These can be extended depending on the case.

Are tax investigations actually getting longer?

HMRC’s own data shows that compliance is a big part of their operations. In 2024/25, they generated roughly£3.7 billion in additional receipts from wealthy individuals. They also spent an estimated £290 million on compliance activity in this group.

While HMRC does not publish a single headline statistic on the average length of investigations into individuals, several clear trends point in the same direction.

First, complex cases take time by design. HMRC’s own National Audit Office reviews have repeatedly acknowledged that investigations involving wealthy individuals are more detailed and resource‑intensive. These cases frequently span multiple tax years, involve international travel patterns, and require extensive evidence gathering. The Gaines-Cooper case is an example of a case that spanned over a decade from investigation to legal conclusion.

Second, HMRC is prioritising quality over speed in high‑risk cases. Dedicated teams, such as the Wealthy and Mid‑Sized Business Compliance directorates, are incentivised to pursue fewer cases more deeply, rather than closing a high volume quickly. That inevitably extends timelines.

Third, data‑led investigations lengthen the process if the records are weak. HMRC’s use of advanced analytics, including its long‑established Connect system, means discrepancies can surface long after the relevant tax year. When an individual is then asked to reconstruct where they were, what they were doing, and why, delays are common.

Finally,HMRC tax investigations paused or slowed during the pandemic years are still working their way through the system. Many advisers report that cases opened several years ago are only now reaching resolution.

The result is not that every investigation lasts longer, but that those involving global mobility and residency often do.

Why Are Wealthy Individuals More Exposed?

HMRC has been explicit about why wealthy individuals receive disproportionate attention. High‑net‑worth tax affairs tend to be:

International in nature

Dependent on factual questions (such as physical presence)

More open to interpretation

Higher value, even where the technical issue is narrow

From HMRC’s perspective, residency and domicile claims are inherently risk‑based. Two people can have similar lifestyles but very different tax outcomes depending on day counts, ties, and evidence. Where that evidence is incomplete or inconsistent, HMRC is far more likely to investigate, and to take its time doing so to get it right.

Crucially, when a tax investigation is launched, it doesn’t necessarily mean there was apparent wrongdoing. Again, the investigation is to establish the truth. Many tax investigations ultimately result in no additional tax being due. Because cases are hardly black-and-white, tax investigations, by nature, can drag on.

What Actually Makes Investigations Drag On

As we eluded above, the length of an investigation is rarely driven by a single factor. More often, it is a combination of avoidable issues:

Reconstructing historical day counts years after the event

Inconsistent records across advisors, calendars, and spreadsheets

Over‑reliance on indirect evidence, such as credit card statements or emails

Manual processes that slow responses to HMRC information requests

Unclear narratives about travel, work, and personal ties

Delays tend to arise when individuals and their advisors must piece together evidence retrospectively, sometimes going back a decade or more.

This is where investigations become emotionally draining, not because of feelings of guilt but because the sheer weight of proving your innocence is draining. While the administrative burden often falls solely on tax advisors, both advisors and individuals feel pressure to resolve the situation as quickly as possible.

How strong compliance records shorten investigations

One of the least appreciated aspects of HMRC tax investigations is that good records not only reduce risk but also minimise duration.

When HMRC receives:

A straightforward, consistent day‑count narrative

Contemporaneous records rather than reconstructed estimates

Evidence that aligns with location data

Information presented in a structured, accessible format

…the scope of questioning often narrows quickly.

Investigations stall when HMRC has to keep asking follow‑up questions, challenge assumptions, or test alternative explanations. They move faster when the facts are already organised and defensible.

This is particularly true for residency cases, where the question is not simply how much time the individual spent in a tax jurisdiction, but whether they can prove those days with evidence.

The Role of Automation and Technology

For many years, day counting has been treated as an administrative afterthought. Advisors gave excellent advice on why day counting matters, but clients were left without a clear process to follow. Day counts were tracked manually and reviewed once a year. That approach is increasingly out of step with how tax authorities operate.

Automated technology changes the dynamic in three critical ways.

First, it creates contemporaneous records. Location data captured in real time is inherently more reliable than a spreadsheet updated months later.

Second, it links day counts to evidence. Photographs, notes, and supporting documents tied directly to specific dates and locations provide context that HMRC increasingly expects.

Third, it reduces friction during an investigation. When information can be exported, reviewed, and shared quickly with advisors, response times improve dramatically.

The goal is to remove ambiguity and have the confidence to state to HMRC, “There’s nothing to see here, everything is in order”.

For advisors, this shifts investigations away from reactive reconstruction and back towards structured, defensible engagement with HMRC.

Reducing Stress, Not Just Risk

One of the less discussed consequences of a lengthy tax investigation is the personal toll it can take. Even where no additional tax is ultimately due, prolonged uncertainty can affect decision-making, travel plans, and peace of mind.

Strong compliance systems do not prevent every enquiry nor should that be the expectation. What they can do, however, is:

Shorten the overall duration of an investigation

Reduce professional fees by limiting reconstruction work

Minimise disruption to daily life and future planning

Allow advisors to focus on strategy rather than administration

In that sense, good compliance is about preserving time, clarity, and confidence when scrutiny arises.

FAQs - HMRC tax investigations

How long does an HMRC tax investigation take?

An HMRC investigation can last months to several years, depending on complexity and the quality of records. Straightforward aspect enquiries may resolve faster, while cross-border, residency, or multi-year matters typically take longer.

What triggers an HMRC tax investigation into an individual?

Common triggers include inconsistencies in returns, lifestyle or asset data not matching declared income, offshore connections, and complex residency or domicile positions. HMRC also uses data-matching tools to identify anomalies that can prompt further checks.

Can HMRC investigate you even if you’ve done nothing wrong?

Yes. HMRC investigations are launched to establish facts in an unclear situation. Many cases conclude with no additional tax due, but the process can still be time-consuming if records are incomplete or need to be reconstructed.

Final thoughts

HMRC tax investigations into individuals are not new, and they are not something to panic about. But for high-net-worth and globally mobile individuals, they are increasingly detailed and can easily drag on longer than a few months.

The difference between a contained tax enquiry and a multi-year ordeal often comes down to preparation. Transparent narratives, contemporaneous records, and well-structured evidence can significantly reduce both the scope and the duration of HMRC’s questions.

For advisors supporting high-net-worth and globally mobile clients, reviewing record-keeping and day-count processes before an enquiry begins can make a meaningful difference – both to outcomes and to the experience of managing the investigation.

If you’d like to explore how you can provide an automated, effective compliance process for your clients and add value to your firm’s service offerings, book a call with our team today.

Discover how to be tax compliant with Daysium

Created in partnership with industry experts, tackle the complex challenges of day counting and tax record-keeping.

Receiving a letter from HMRC is rarely the beginning of the story. By the time it lands, they already know more than most taxpayers expect. We sat down with Daysium Founding Partner and the Founder of UK’s Contentious Tax Group, Sarah Scala, to unravel what a tax inquiry looks like, and why what you do before it matters most.

The Temporary Repatriation Facility gives former remittance basis users a window to pay a reduced rate on pre-April 2025 foreign income and gains, but only for a three-year window that closes in 2028. For globally mobile individuals, the strength of your historical tax residency records is vital to withstand HMRC scrutiny.

Most tax residency positions are technically sound. The vulnerability lies in the records that would need to support them under scrutiny. This guide helps advisors identify where client record-keeping risks are most likely to emerge, and what to do about.

As an HNWI and globally mobile individual, you’re likely to come across HMRC nudge letters. But what are they, why they’re sent, who might receive one, and what are the practical steps to take with a tax advisor to prevent escalation?